How to file tax returns for your SA business in 2026

Executive Summary

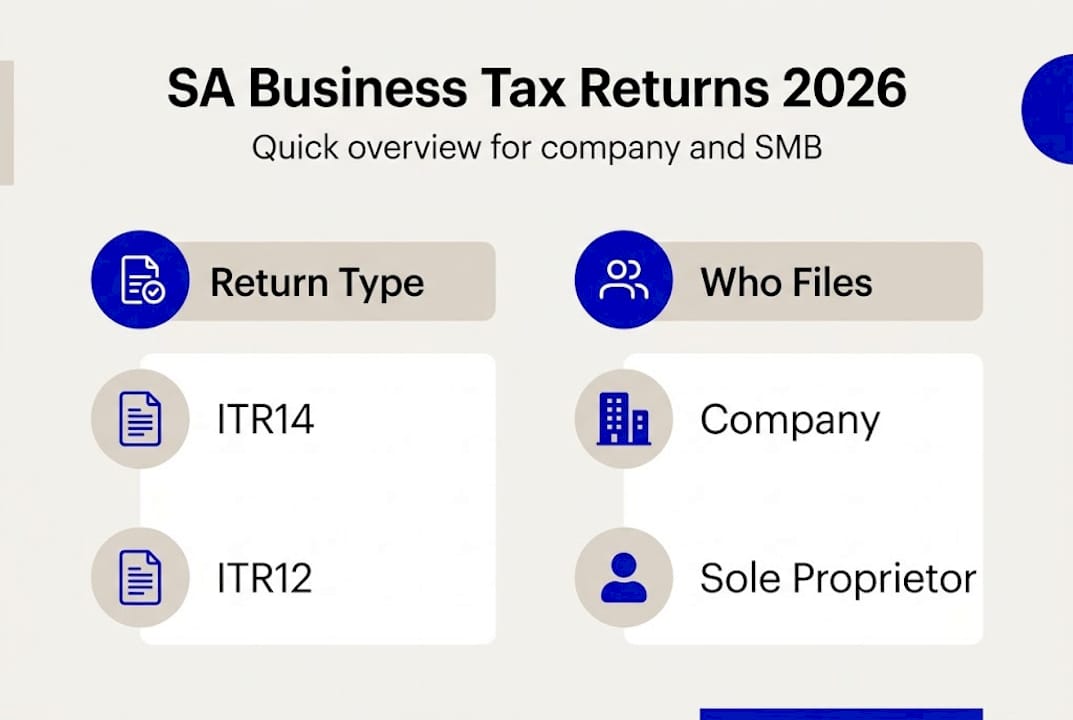

- Different business structures require specific SARS tax returns, such as ITR14 for companies and ITR12 for sole proprietors.

- Accurate record-keeping for five years is essential to ensure compliance and avoid penalties during audits.

- Choosing the right tax regime and using digital tools simplify filing, reduce errors, and lower audit risk.

Filing a business tax return feels manageable until you’re staring at a SARS eFiling screen with no idea which form to complete or whether your records will survive an audit. For South African SMBs, the stakes are real: late or incorrect submissions can trigger penalties of up to 200% of the tax owed. This guide walks you through every step, from identifying the right return for your business structure, to gathering your documents, submitting on eFiling, and optimising your filing to keep your effective tax rate as low as legally possible. Follow each section and compliance stops being a burden.

Table of Contents

- Understand your business tax return requirements

- Get your records and documents ready

- Step-by-step: Register and file your return with SARS eFiling

- Optimize your filing: Minimize penalties and boost compliance

- What most guides miss about SMB tax filing in South Africa

- Ready Accounting: Your partner for painless tax compliance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Choose the correct return | Your business type and turnover determine if you file ITR14, ITR12, IRP6, or TT03. |

| Keep records for 5 years | Organized financial documents are essential for SARS compliance and audit protection. |

| Register and use SARS eFiling | Online submission simplifies filing, but accurate data and deadlines are critical. |

| Optimize regime and estimates | Eligible SMBs can lower tax rates and avoid penalties by selecting the right regime and making accurate provisional payments. |

| Prepare for audits proactively | SARS’s increasing audit focus means SMBs must prioritize compliance and readiness every year. |

Understand your business tax return requirements

Not every business files the same return, and mixing them up is one of the most common and costly mistakes South African SMB owners make. Your business structure determines which form you need, which deadlines apply, and whether you qualify for a simplified, lower-rate regime.

Here is a quick overview of the main return types:

| Business type | Return to file | Notes |

|---|---|---|

| Registered company (Pty Ltd, CC) | ITR14 | Annual income tax return |

| Sole proprietor / individual | ITR12 | Filed as part of personal income tax |

| Provisional taxpayer | IRP6 | Filed twice a year (first and second provisional) |

| Micro business (Turnover Tax) | TT03 | Annual; register with TT01 first |

SMBs file ITR14 for companies, ITR12 for sole proprietors, and IRP6 for provisional taxpayers. If you run a registered company, the ITR14 is your primary annual return. Sole proprietors declare business income on their personal ITR12. Provisional taxpayers, which includes most SMB owners who earn income beyond a salary, must also submit IRP6 returns twice per year.

For very small businesses, there is a compelling alternative. Micro businesses can opt for Turnover Tax and file a TT03 annually rather than the standard corporate tax route. To qualify, your annual turnover must be below R1 million. Turnover Tax replaces income tax, VAT, provisional tax, and capital gains tax with a single simplified rate, making compliance significantly simpler.

A few edge cases worth knowing:

- Dormant companies still need to file an ITR14, even with zero income.

- If your turnover drops below the Turnover Tax threshold, you can deregister and switch regimes.

- Small Business Corporations (SBCs) file a standard ITR14 but benefit from graduated tax rates starting at 0% on the first R95,750 of taxable income in 2026.

For a deeper look at which regime suits your situation, the income tax return guide on our site breaks down each option clearly. You can also find a broader overview in the small business tax overview covering rates and thresholds. SARS also publishes its own SARS small business taxpayer resources as a reference point.

Pro Tip: The Turnover Tax regime suits businesses with simple cost structures and high turnover relative to net profit. If your margins are thin, standard corporate tax with expense deductions might actually be cheaper. Run both calculations before committing.

Get your records and documents ready

Once you have confirmed your filing requirements, gather the necessary documentation before logging into eFiling. Walking into the filing process without your records is the fastest way to submit inaccurate figures and invite an audit.

Here is the core checklist of what you need:

- Annual financial statements (income statement and balance sheet)

- IRP5 certificates for employees and directors

- Bank statements for the full tax year

- All invoices issued and received

- Loan agreements and interest schedules

- Asset registers for depreciation calculations

- Supporting schedules: capital gains, foreign income, assessed losses

Records must be kept for 5 years; SARS conducts intensive audits and can request documentation from any year within that window. Failing to produce records means SARS can estimate your liability, which is almost always unfavourable to you.

Here is a practical breakdown of mandatory versus recommended documents:

| Document | Status | Purpose |

|---|---|---|

| Annual financial statements | Mandatory | Core return completion |

| Bank statements (12 months) | Mandatory | Income and expense verification |

| IRP5 / IT3(a) certificates | Mandatory | Employee tax reconciliation |

| Invoices and receipts | Mandatory | Audit evidence |

| Asset register | Recommended | Depreciation and Section 12C claims |

| Loan schedules | Recommended | Interest deduction support |

| Prior year return | Recommended | Assessed loss carry-forward |

Accurate records also make the eFiling process faster. SARS pre-populates some fields on the ITR14 using third-party data it receives from banks and employers. If your records do not match those pre-populated values, you will need to explain the difference, and that explanation must be backed by documentation.

For detailed guidance on what SARS expects, review the record-keeping rules that apply to your business type, as well as the record keeping requirements that came into effect for 2025 onward.

Pro Tip: Cloud accounting software like Xero or QuickBooks Online automatically stores invoices, bank feeds, and reconciliations in one place. When SARS asks for records, you can export exactly what they need in minutes instead of weeks.

Step-by-step: Register and file your return with SARS eFiling

Now that your records are in order, you are ready to file. Here is how to do it step by step.

-

Register on SARS eFiling. Go to efiling.sars.gov.za. If you are a new user, create an account and link your business tax number. Existing users should verify their registered details, especially the banking information, contact details, and representative taxpayer.

-

Select the correct return. Under the “Returns” menu, choose the return that applies: ITR14 for companies, ITR12 for individuals, IRP6 for provisional tax, or TT03 for Turnover Tax. Register on eFiling, verify details, complete returns is the official SARS guidance for the ITR14 specifically.

-

Complete the return fields. For the ITR14, you will work through sections covering income, deductions, capital allowances, and assessable amounts. The system is question-driven, meaning certain sections only appear if you answer “yes” to a trigger question. Answer carefully. For IRP6, you estimate your taxable income for the period and calculate the provisional payment due.

-

Upload supporting documents if prompted. SARS may request supporting documents during submission for higher-risk returns. Have your financial statements in PDF format ready to upload.

-

Review, calculate, and submit. Use the “Calculate” function before submitting to see the tax liability. Cross-check this against your own calculations. If the numbers differ significantly, stop and investigate before submitting.

-

Pay any tax due. If a payment is required, use the eFiling payment portal or your bank’s SARS payment option. Use the correct payment reference number to ensure the payment is allocated correctly.

For a broader view of how filing fits into your annual financial calendar, the year-end tax planning guide offers a structured timeline. If you have specific questions about your situation, the common tax questions resource addresses the most frequent issues SMBs encounter. The SAIT tax filing tutorial is also a reliable external reference.

Warning: Late submission of the ITR14 or IRP6 triggers an automatic administrative penalty. Underestimating your provisional tax by more than 20% of the actual liability results in a penalty on the shortfall. Filing on time and accurately is non-negotiable.

Pro Tip: Many accounting software packages support direct integration with SARS eFiling through a trial balance export or an XML upload. If your software supports this, use it. It eliminates manual data entry errors and cuts filing time significantly.

Optimize your filing: Minimize penalties and boost compliance

You have submitted your returns. Now focus on avoiding mistakes and optimising your filing for future periods.

The single biggest lever available to most SMBs is regime selection. Choosing Turnover Tax or SBC if eligible delivers lower effective rates and simpler compliance. Here is how to think about each option:

- Standard company rate: 27% flat on taxable income (2026). No special requirements.

- Small Business Corporation (SBC): Graduated rates starting at 0% up to R95,750, then 7%, 21%, and 27% on higher bands. Requires meeting specific shareholder and gross income tests.

- Turnover Tax: Rates from 0% to 3% of turnover. Replaces most other taxes. Requires annual turnover under R1 million.

Accurate provisional tax estimates are equally critical. SARS calculates penalties based on the difference between your estimate and the final assessed liability. If your estimate falls short by more than the allowed 20% tolerance, the penalty applies automatically, no discretion involved.

Audit readiness checklist:

- Keep all source documents (not just summaries) for 5 years

- Reconcile your VAT returns against your income tax return figures

- Ensure your IRP5 values match your payroll records exactly

- Flag any related-party transactions and document them at arm’s length

- Cash-intensive businesses face higher scrutiny; maintain a daily cash-up register

SARS audit reality: SARS conducted over 11,000 audits in a recent compliance cycle, recovering R8.3 billion. Cash businesses and SMBs with inconsistent filings are the primary targets.

For strategies to legally reduce your tax burden, visit our smart tax savings guide. If you have already received a penalty notice, the avoiding tax penalties guide explains your options. SARS also publishes SARS optimization rules for businesses considering regime changes.

Pro Tip: If your business had an unusual year, such as a large asset sale, a new loan, or a significant drop in revenue, consult a tax professional before submitting your provisional return. Getting the estimate right the first time is far cheaper than correcting it afterward.

What most guides miss about SMB tax filing in South Africa

Most filing guides focus on the mechanics: which form, which deadline, which button to click. That is useful, but it misses the bigger picture entirely.

The SMBs we work with that handle SARS best are not necessarily the ones who file perfectly every year. They are the ones who made a deliberate choice about their tax regime, invested in cloud accounting tools early, and built an audit-ready mindset long before SARS ever came knocking. Choosing the right regime and digital tools can make filing painless and significantly boost audit readiness.

Most SMB owners dramatically underestimate audit risk. SARS is not passively waiting for errors to surface. Its systems actively cross-reference your return against bank data, VAT submissions, and third-party information. The question is not whether SARS can see a discrepancy. It is whether your records can explain it.

We also see businesses delay switching to more efficient tax structures because the process feels complicated. It does not have to be. The sooner you assess your regime fit, the more you save.

“A proactive approach is your best insurance against costly mistakes. Filing correctly once is always cheaper than fixing errors under audit pressure.”

Ready Accounting: Your partner for painless tax compliance

When you are ready to get practical help, Ready Accounting makes tax filing far less stressful. Our cloud-based bookkeeping and tax consulting services are built specifically for South African SMBs who need accurate records, timely submissions, and expert advice on regime optimisation.

We use cloud accounting benefits to keep your financial records audit-ready throughout the year, not just at filing time. Our team also guides you through the full tax compliance guide process, from provisional tax estimates to final ITR14 submission. Whether you are a sole proprietor filing your first ITR12 or a growing company considering SBC status, we give you the expert support to file correctly and confidently. Book a consultation today and take tax stress off your plate.

Frequently asked questions

Which SARS form does my business need to file?

Most companies must file an ITR14, sole proprietors use an ITR12, and provisional taxpayers submit an IRP6. SMBs file ITR14, ITR12, IRP6; micro businesses opting for Turnover Tax file a TT03 instead.

What records must I keep for SARS and for how long?

You must keep financial records, invoices, and bank statements for at least 5 years after the relevant tax year. SARS requires 5-year record retention and can request any documents within that window during an audit.

How do provisional tax deadlines work for South African SMBs?

You must file your IRP6 twice per year based on your business year-end, submitting estimates of taxable income and paying the amount due before each deadline. IRP6 provisional returns are submitted at the six-month and year-end marks of your financial year.

Can I reduce my business’s tax rate by changing how I file?

Yes, qualifying for Small Business Corporation status or Turnover Tax gives you access to graduated rates that are significantly lower than the standard 27% corporate rate. SBC and Turnover Tax offer lower rates if your business meets the eligibility criteria.

What happens if I file late or underestimate my provisional tax?

SARS imposes automatic administrative penalties for late filing, and inaccurate provisional estimates can attract penalties of up to 200% for serious understatement. Penalties for understatement can reach 200%, making accuracy a financial priority, not just a compliance one.

Recommended

- Year-End Tax Planning Guide for Small Businesses - Ready Accounting

- Top Tax Questions Small Business Owners Ask in 2025 - Ready Accounting

- Income tax returns for SA SMEs: What owners must know - Ready Accounting

- Tax efficient structures for South African SMBs in 2026 - Ready Accounting

- Navigate digital tax trends: a 2026 guide for sole traders