Mastering profit and loss for smarter business decisions

Executive Summary

- South African SMBs operate with very thin profit margins averaging 1.3 percent.

- Regularly reviewing and analyzing the profit and loss statement is essential for business survival and growth.

- Proper understanding and application of accounting methods impact financial visibility and compliance.

South African businesses operate on some of the thinnest profit margins in the world. Thin profit margins averaged just 1.3% after tax in 2024, meaning a single bad month can wipe out an entire year’s gains. Yet many small and medium business owners still treat their profit and loss statement as a once-a-year document they hand to their accountant without a second glance. That is a costly habit. This guide will walk you through what a P&L statement actually is, how to read each line, which accounting method applies to your business, and how to turn those numbers into decisions that keep your business alive and growing.

Table of Contents

- What is a profit and loss statement and why does it matter?

- Breaking down the components of profit and loss

- Cash vs accrual basis: How do methods impact your P&L?

- How to use your P&L for better business decisions

- The uncomfortable truth about profit and loss for South African SMBs

- Take your financial understanding further with expert support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your numbers | Understanding your P&L empowers better business decisions under tough economic conditions. |

| Choose the right method | Selecting the proper accounting basis ensures accurate profit reporting and legal compliance. |

| Review regularly | Monthly P&L checks help spot issues early, before they threaten your business. |

| Profit is not cash | Positive profits don’t guarantee cash flow—monitor both to avoid insolvency. |

| Use P&L for growth | Apply P&L insights proactively for budgeting, funding, and operational resilience. |

What is a profit and loss statement and why does it matter?

A profit and loss statement, also called an income statement, is a financial report that summarises your revenue, costs, and expenses over a specific period. Think of it as your business’s report card. It tells you whether you made money or lost it, and it shows exactly where money came in and where it went out.

Unlike a bank statement, a P&L is structured to show cause and effect. It does not just say you have R15,000 in your account. It explains whether you earned R200,000, spent R185,000, and arrived at R15,000 in net profit. That context is what makes it powerful.

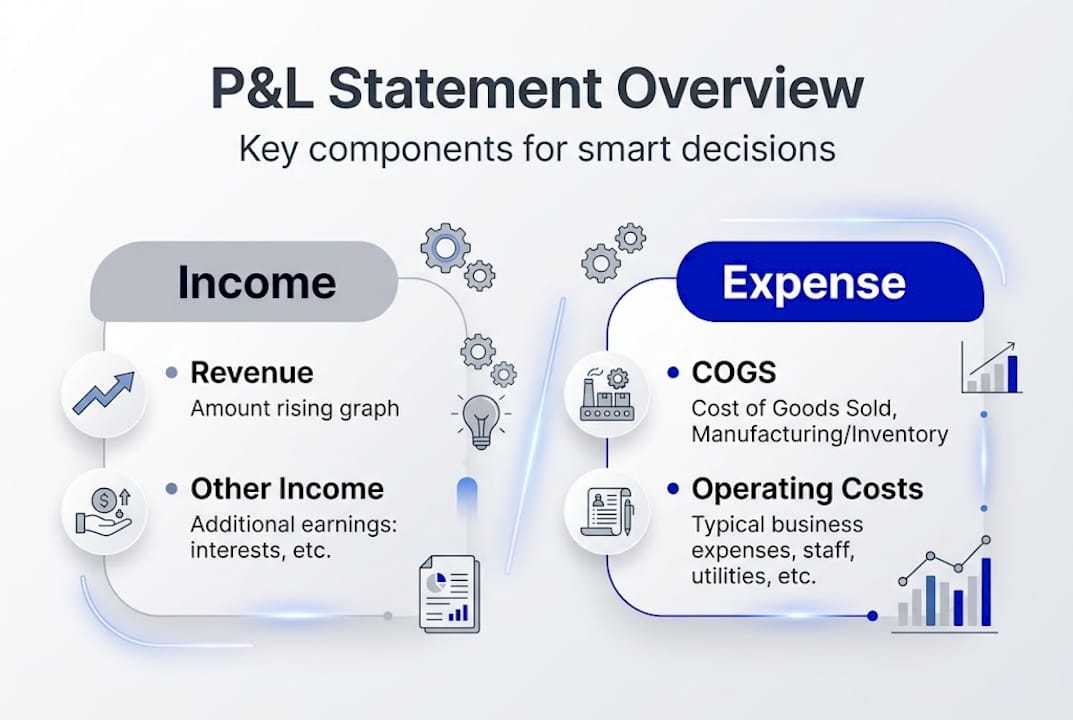

The key components of a P&L statement include:

- Revenue (net sales): Total income generated from your products or services

- Cost of Goods Sold (COGS): Direct costs tied to producing what you sell

- Gross Profit: Revenue minus COGS

- Operating Expenses: Rent, salaries, marketing, and other overhead costs

- Operating Income: Gross profit minus operating expenses

- Other Income or Expenses: Interest, one-off items, or non-operating transactions

- Net Profit: What remains after all costs and taxes are deducted

For South African SMBs, understanding income statement basics is not a nice-to-have skill. It is a survival skill. Your P&L is the document banks want when you apply for funding, SARS scrutinises when you file taxes, and investors examine when you pitch for capital.

A common misconception is that profit means cash in the bank. It does not. You can show a healthy profit on paper while struggling to pay suppliers next week. This is one of the most dangerous traps for growing businesses. Another misconception is that a P&L only matters at year-end. In reality, financial statement fundamentals tell you that reviewing your P&L monthly gives you enough time to course-correct before small problems become serious ones.

Pro Tip: If your gross profit is healthy but your net profit is shrinking, look hard at your operating expenses. That gap is where most small businesses bleed money without noticing.

Your P&L also aids decision-making, budgeting, cash flow management, loan applications, and tax filing. It is the single most versatile financial document your business produces.

Breaking down the components of profit and loss

Let us walk through each P&L component using a practical example of a South African retail shop turning over R500,000 per year.

The P&L components work together in a logical sequence. Each line builds on the one above it, so an error or misclassification early on distorts every figure below. Here is how they stack up:

- Revenue: Your shop earns R500,000 from product sales. This is the starting point. Returns or discounts are deducted here to give you net sales.

- COGS: You paid R300,000 for the stock you sold. This is a direct cost, meaning it moves with your sales volume.

- Gross Profit: R500,000 minus R300,000 equals R200,000. This shows how efficiently you are producing or sourcing what you sell.

- Operating Expenses: Rent, salaries, utilities, and marketing total R160,000. These are fixed or semi-fixed costs that exist regardless of sales.

- Operating Income: R200,000 minus R160,000 equals R40,000. This tells you how profitable your core operations are.

- Net Profit: After accounting for interest on a business loan and income tax, you are left with R28,000. This is your actual bottom line.

| P&L component | Definition | Example ® |

|---|---|---|

| Revenue | Total income from sales | 500,000 |

| COGS | Direct cost of goods sold | 300,000 |

| Gross Profit | Revenue minus COGS | 200,000 |

| Operating Expenses | Overhead and admin costs | 160,000 |

| Operating Income | Gross profit minus expenses | 40,000 |

| Net Profit | After taxes and interest | 28,000 |

The difference between gross profit and net profit is critical. Gross profit tells you if your pricing model works. Net profit tells you if your entire business model works. You can have a healthy gross margin of 40% and still lose money if your overheads are out of control.

Visit sample financial statements to see how real South African businesses structure these figures. Common mistakes include putting owner drawings under expenses, mixing personal and business costs, or misclassifying COGS as an operating expense. Each of these distorts your gross profit figure and hides the real performance of your business.

Pro Tip: Track your gross profit margin as a percentage, not just a rand value. If your margin drops from 40% to 35% over three months, you need to find out why before you look at calculating gross profit targets for the next quarter.

Cash vs accrual basis: How do methods impact your P&L?

Here is something many business owners discover too late: two businesses with identical transactions can report completely different profits depending on the accounting method they use. The choice between cash basis and accrual basis changes what appears on your P&L, and when.

Cash basis records income when money is received and expenses when they are paid. If you invoice a client in March but they pay in May, that income only appears on your May P&L. It is simple and mirrors your bank account, which is why smaller operations prefer it.

Accrual basis records income when it is earned and expenses when they are incurred, regardless of cash movement. That March invoice appears on your March P&L. This gives a more accurate picture of how your business performed during that period.

| Factor | Cash basis | Accrual basis |

|---|---|---|

| When income is recorded | Cash received | Invoice raised |

| When expenses are recorded | Cash paid | Cost incurred |

| Best suited for | Micro businesses under R2.5M | Growing SMBs and VAT vendors |

| SA compliance requirement | Optional below R2.5M turnover | Required above R2.5M turnover |

| Loan and investor appeal | Lower | Higher |

Accrual accounting is required for businesses with turnover above R2.5 million or those registered on the VAT invoice basis. This is not optional. SARS expects your financial records to match the method appropriate to your size and VAT status.

Research into accounting method impacts confirms that cash basis is simpler for small operations but can distort performance visibility, while accrual is more accurate for growth decisions but adds administrative complexity.

The risk of choosing the wrong method is real. If you use cash basis when accrual is required, your annual financial statements may not comply with SARS requirements, which creates problems during audits and tax submissions. It can also mislead you into thinking you are more or less profitable than you actually are.

- Using cash basis when clients pay late makes your business look unprofitable in busy months

- Accrual can show high profit while your bank account sits empty, creating cash flow blind spots

- Switching methods mid-year without professional guidance creates reconciliation nightmares

How to use your P&L for better business decisions

A P&L statement only adds value when you act on what it shows. Too many South African SMB owners treat it as a compliance document rather than a decision-making tool. Here is how to change that.

- Run monthly reviews: Compare each month to the same month last year. Seasonal patterns, cost creep, and declining margins all become visible when you look at trends rather than single snapshots.

- Set gross margin benchmarks: Know your industry’s typical gross margin and measure yourself against it. If you fall below your benchmark for two consecutive months, investigate immediately.

- Watch your expense-to-revenue ratio: If expenses grow faster than revenue, your net profit will shrink even as sales increase. This is a common trap in expansion phases.

- Use P&L for funding conversations: Banks and alternative lenders want to see at least 12 months of P&L history. A clean, consistent record signals that your business is well-managed.

- Identify your most and least profitable lines: Break your revenue into product or service categories. Some lines may carry high revenue but thin margins, dragging down overall profitability.

The P&L’s role in budgeting, loan applications, and tax filing makes it one of the most practical tools you have. With South African SMEs reporting a 50% drop in turnover in 2024 and significant job losses across the sector, having a clear and current P&L is no longer optional for survival.

“The businesses that survive economic downturns are not always the most profitable. They are the ones that catch problems early enough to respond.”

Learning to read financial statements and then analyzing your P&L for red flags are two skills that can genuinely protect your business during tough trading periods.

The uncomfortable truth about profit and loss for South African SMBs

Most business owners we work with know their monthly revenue figure off the top of their heads. Very few know their gross margin to the same precision. That gap is where businesses quietly fail.

The uncomfortable reality is that your P&L is a starting point, not a finish line. South Africa’s thin average margins of 1.3% mean there is almost no room for error. Owners who review their P&L once a year are essentially flying blind for eleven months. By the time they spot a problem, the damage is done.

The savvy owners we see thriving in 2026 do three things differently. They review their P&L every month without exception. They track cash flow alongside profit because they know a profitable business can still become insolvent. And they focus on margin trends, not just absolute figures. A rand increase in profit is meaningless if your margin is shrinking because costs are rising faster than revenue.

Monitoring business financial health indicators alongside your P&L gives you a much fuller picture of where your business actually stands. Stop treating profit as the only number that matters. Start treating your P&L as a monthly management conversation with your business.

Take your financial understanding further with expert support

Understanding your profit and loss statement is a critical first step, but applying those insights consistently takes time and skill that most business owners simply do not have spare. At Ready Accounting, we help South African SMBs turn raw financial data into clear, actionable decisions through tailored accounting support and smart automation tools. Whether you are exploring the benefits of a cloud accounting guide to streamline your bookkeeping, or want to understand the cloud accounting benefits for your specific business model, our team is ready to help. Visit Ready Accounting to book a consultation and start managing your numbers with confidence.

Frequently asked questions

What is the difference between profit and cash flow in my business?

Profit tracks income minus expenses over a period, while cash flow measures actual money moving in and out. You can show a healthy profit and still run out of cash if clients pay late or expenses fall due at the wrong time, which is why thin margins make cash flow monitoring as important as profit tracking.

Do I need to use accrual accounting for my South African small business?

If your annual turnover exceeds R2.5 million or you use VAT invoice accounting, accrual is required by SARS. Below that threshold, cash basis accounting is an option but may limit your ability to attract funding or present accurate financial performance.

How often should I review my profit and loss statement?

Review your P&L at least monthly. With average after-tax margins as thin as 1.3%, a quarterly review leaves too much time for problems to grow before you catch them.

Why is my P&L important for loan and tax applications?

Lenders and SARS use your P&L to verify income, assess expense patterns, and confirm consistent profitability. A well-maintained P&L for applications dramatically improves your chances of funding approval and smooth tax submissions.