Auditing financial statements: protocol for South African Corporate Assets

Executive Summary

- Financial statements provide a complete picture of a business’s financial health and performance.

- South African SMBs must prepare and submit annual financial statements within six months of year-end.

- Regular, timely review of key financial ratios enables early detection of liquidity and profitability issues.

Some businesses post their best sales month ever, then struggle to pay salaries two weeks later. It feels wrong, but it happens constantly. The gap between sales and actual financial health is exactly what financial statements reveal. For small and medium business owners in South Africa, understanding your numbers is not optional. It is the difference between growing with confidence and making decisions in the dark. This guide walks you through what financial statements are, the types you need, what the law requires, how to prepare them, and how to use them to spot problems before they become crises.

Table of Contents

- What is a financial statement and why does it matter?

- Types of financial statements every SMB needs to know

- Financial statement compliance in South Africa: Rules, deadlines, and standards

- How to prepare and analyse your financial statements

- A practical perspective: Why simple, timely financials are your best tool

- Take the next step: Get expert help and modern tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Legal requirements | South African SMBs must prepare annual income, balance sheet, cash flow, and notes for CIPC and tax compliance. |

| Business insights | Using financial statements monthly helps owners spot cash flow problems, rising debt, and profit trends early. |

| Types of statements | All SMBs need at least three core reports: income statement, balance sheet, and cash flow statement. |

| Analysis methods | Understanding ratios like current, quick, and debt-to-equity is key to healthy business finances. |

| Simpler is better | Practical, timely financial statements are more valuable than perfect but late reports for SMBs. |

What is a financial statement and why does it matter?

A financial statement is a structured report that captures what your business owns, owes, earns, and spends over a specific period. Think of it as your business’s medical file. Just as a doctor cannot treat a patient without test results, you cannot run a healthy business without reliable numbers. Financial statements are formal records that provide a complete overview of a business’s health, position, and cash flows.

These records serve several important purposes. They help you make informed decisions about spending, hiring, and expansion. They show banks and investors whether your business is worth funding. They satisfy legal reporting requirements under the Companies Act 2008. And they give SARS the information needed to assess your tax obligations. See examples of financial statements to understand what a complete set looks like in practice.

Who actually reads your financial statements? More people than you might think:

- You, the owner: To understand profitability and cash flow

- Banks and lenders: To assess creditworthiness before approving loans

- Investors: To evaluate return potential before committing capital

- SARS: To verify tax calculations and compliance

- CIPC: To confirm annual filing obligations are met

- Auditors and accountants: To review accuracy and flag risks

Neglecting accurate statements carries real consequences. Poor or missing financials can block access to funding, lead to incorrect tax submissions, result in CIPC penalties, and leave you flying blind when making major business decisions. A solid financial reporting guide can help you understand what is required and why each component matters.

“Accurate financial statements are not just a compliance exercise. They are the clearest window into whether your business is actually working.”

Many owners only look at their bank balance. That tells you almost nothing about the true state of your business.

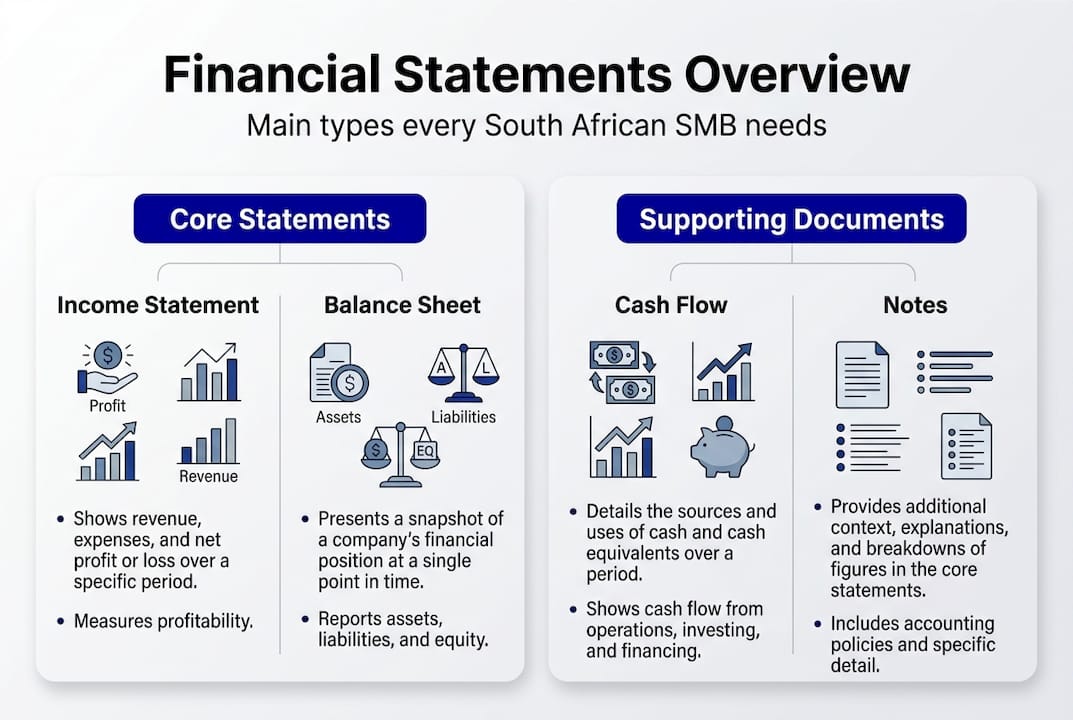

Types of financial statements every SMB needs to know

Most business owners have heard of an income statement, but a complete financial picture requires more than one document. South African SMBs need to understand three core statements, plus supporting documents required under local law.

Here is a quick overview of the core statements every business should prepare:

| Statement | Main sections | Key question it answers |

|---|---|---|

| Income statement | Revenue, expenses, net profit/loss | Is the business profitable? |

| Balance sheet | Assets, liabilities, equity | What does the business own and owe? |

| Cash flow statement | Operating, investing, financing flows | Does the business have enough cash? |

Each statement plays a distinct role. The income statement breakdown shows whether your operations are generating profit after all costs. The balance sheet reveals financial stability, showing whether your assets outweigh your liabilities. The cash flow statement is often the most overlooked, yet it explains why a profitable business can still run out of cash.

Why each one matters:

- Income statement: Tracks profitability over time and identifies cost problems

- Balance sheet: Shows whether you are building or eroding business value

- Cash flow statement: Flags liquidity risks before they become emergencies

- Statement of changes in equity: Required under South African law, it tracks how owner equity shifts over the year

- Notes to the financial statements: Provide context, accounting policies, and disclosures required by your reporting standard

South African SMBs must also stay aware of the types of financial statements required under current standards. Most SMBs report under IFRS for SMEs. The IFRS for SMEs 2025 standards introduce a third edition effective from 2027, bringing updates to revenue recognition, fair value measurement, and note disclosures. If you are reading financial statements for the first time, start with the income statement and cash flow statement. They tell the most immediate story.

Financial statement compliance in South Africa: Rules, deadlines, and standards

Understanding the types is one thing, but as a local business, what do you actually need to prepare and when? South African law is specific, and missing deadlines has consequences.

SMBs must prepare Annual Financial Statements per the Companies Act 2008, within six months of their financial year-end, and submit these to CIPC. For a business with a February year-end, that means statements must be ready by August. Late submissions attract penalties and can affect your company’s good standing.

Here are the steps to stay compliant:

- Appoint a qualified accountant or auditor based on your company’s public interest score

- Choose your reporting standard (IFRS for SMEs applies to most private SMBs)

- Gather all supporting records including invoices, bank statements, and payroll data

- Prepare statements within the six-month window after your year-end

- Review notes and disclosures for completeness, especially related party transactions

- Submit to CIPC and retain copies for SARS and internal use

Most SMBs report under IFRS for SMEs rather than full IFRS or SA GAAP, which was phased out. The IFRS for SMEs 2025 update introduces a new five-step revenue model, revised fair value guidance, and stronger requirements around notes and related party disclosures, all effective from 2027. Start preparing now. Waiting until 2027 to understand these changes is a risk you do not need to take.

Check the annual financial statement deadlines relevant to your company type and review tax questions for SMBs that often arise during the preparation process.

For guidance on annual statement formatting, use a checklist to verify that all required sections are present before submission.

Pro Tip: Document your accounting policies for loans, revenue recognition, and depreciation at the start of each financial year. These are the three areas most commonly flagged during CIPC reviews and SARS audits.

How to prepare and analyse your financial statements

With rules clear, let’s roll up our sleeves. Here is how you actually prepare and use your statements to make better decisions.

Preparation starts with gathering records: invoices, bank statements, expense receipts, payroll records, and loan agreements. These feed into your accounting system, where transactions are classified into the correct accounts. An accountant then reviews the output, applies your accounting policies, and produces the final statements.

| Approach | Pros | Cons |

|---|---|---|

| DIY preparation | Low cost, full control | High error risk, time-consuming |

| Accountant-prepared | Accurate, compliant, expert insight | Higher cost |

| Cloud accounting software | Fast, automated, real-time data | Requires setup and ongoing input |

Once prepared, the real value comes from analysis. Trend analysis and ratio analysis are the two most practical tools for South African SMBs. Trend analysis compares figures across periods to spot growth or decline. Ratio analysis converts raw numbers into meaningful benchmarks.

Key ratios to monitor:

- Current ratio (current assets divided by current liabilities): A healthy range is 1.5 to 2.0

- Quick ratio (liquid assets divided by current liabilities): Above 1.0 means you can cover short-term obligations

- DSO (days sales outstanding): How long it takes to collect payment from customers

- Debt-to-equity ratio: Shows how much of your business is funded by debt versus owner investment

These ratios are exactly what banks and investors check when reviewing funding applications. Review financial statement basics to build your foundation, and use a guide on interpreting financial ratios to understand what the numbers mean in context.

Pro Tip: Set a monthly calendar reminder to review your current ratio and cash flow statement. Catching a liquidity problem three months early gives you time to act. Catching it at year-end often means it is already a crisis.

A practical perspective: Why simple, timely financials are your best tool

Here is something most accountants will not say out loud: the biggest financial mistakes South African SMB owners make are not about wrong numbers. They are about delayed numbers.

Many owners treat financial statements as a once-a-year compliance task, something to hand to an accountant in a panic before the CIPC deadline. But that approach turns a powerful management tool into a historical document. By the time you see the problem, it already happened months ago.

The real value of your financial statement basics is not impressing auditors. It is giving you a regular, honest view of your business so you can make better calls every month. A simple monthly review of your income statement and cash flow statement, even just 30 minutes, will do more for your business than a perfect annual report reviewed once.

Do not let technical jargon paralyse you. You do not need to understand every accounting standard to use your financials well. Start with three numbers: revenue, net profit, and cash on hand. Track them monthly. Ask why they changed. That habit alone puts you ahead of most SMB owners in South Africa.

Take the next step: Get expert help and modern tools

Ready to make your financial statements work for your business? Here is where expert help and the right tools can make the difference.

At Ready Accounting, we help South African SMBs move from financial confusion to confident clarity. Whether you need help with statement preparation, compliance, or understanding what your numbers actually mean, our team combines cloud technology with hands-on expertise. Explore the cloud accounting benefits that make real-time reporting possible for businesses of any size. Use our easy financial statement guide to start reading your reports with confidence, or browse financial statement examples tailored for South African SMEs. Book a free consultation today and let us help you turn your financials into your strongest business tool.

Frequently asked questions

What is the main purpose of a financial statement?

A financial statement gives a complete picture of a business’s financial position and performance to support decisions, attract funding, and meet compliance requirements.

What types of financial statements are required by law in South Africa?

South African SMBs must prepare an income statement, balance sheet, cash flow statement, and notes annually, submitted to CIPC within six months of their financial year-end under the Companies Act 2008.

Which financial ratios should South African businesses monitor?

Focus on the current ratio (1.5 to 2.0 is healthy for SMEs), quick ratio above 1.0, DSO for cash collection speed, and debt-to-equity for solvency.

How often should I prepare or review my financial statements?

Annual statements are legally required, but monthly reviews of your income statement and cash flow statement help you catch problems early and make better decisions throughout the year.

What is changing with IFRS for SMEs in 2027?

The 2025 IFRS for SMEs update introduces a five-step revenue recognition model, revised fair value rules, and stronger note disclosure requirements, all effective from 2027.

Recommended

- What are financial statements: guide for South African SMBs – Ready Accounting

- Examples of financial statements for South African SMEs – Ready Accounting

- How to Read Financial Statements: Easy Guide for 2025 – Ready Accounting

- Financial Statement Basics: A Guide for Business Owners – Ready Accounting