What is deferred tax: a protocol for South African Scaling Companies 2026

Many South African business owners mistakenly believe deferred tax is an immediate tax payment they owe to SARS. In reality, deferred tax arises from temporary differences between accounting and tax treatment of items impacting future tax liabilities. This accounting concept reflects timing differences between when you recognize income or expenses in your financial statements versus when SARS allows you to report them for tax purposes. Understanding deferred tax is essential for accurate financial reporting, strategic tax planning, and maintaining compliance with South African tax regulations in 2026. This guide clarifies what deferred tax means for your SME and how to manage it effectively.

Table of Contents

- What Is Deferred Tax And Why Does It Matter?

- How To Identify And Calculate Deferred Tax

- Deferred Tax Under South African Tax Rules: Important Considerations

- Managing Deferred Tax For Effective Financial Planning And Compliance

- How Ready Accounting Can Simplify Your Deferred Tax Management

- Frequently Asked Questions About Deferred Tax

Key takeaways

| Point | Details |

|---|---|

| Timing differences | Deferred tax results from differences between when transactions affect accounting profit versus taxable profit |

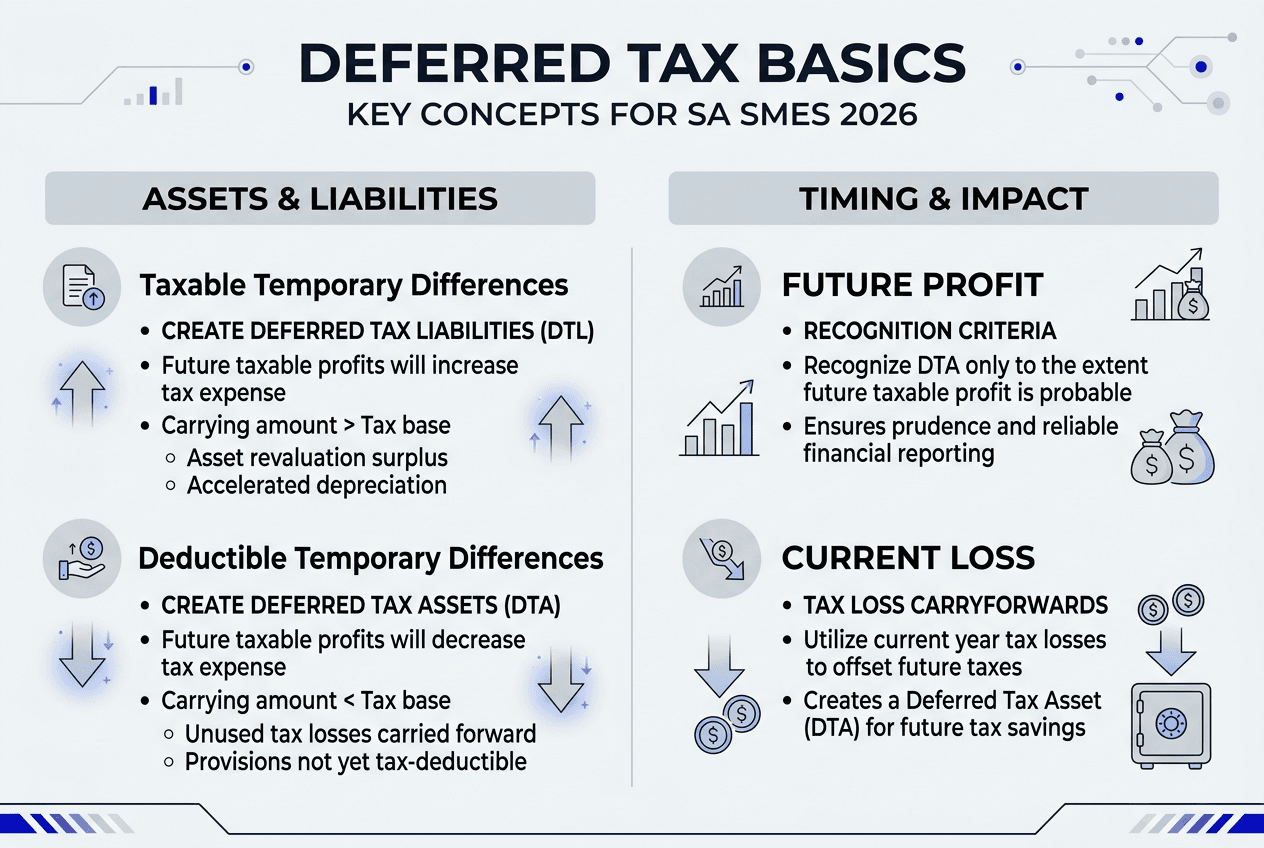

| Assets and liabilities | Deductible differences create deferred tax assets while taxable differences create deferred tax liabilities |

| South African rates | Calculate deferred tax using the 27% corporate tax rate applicable in 2026 |

| Cash flow impact | Deferred tax affects financial reporting but does not represent immediate cash payments to SARS |

| Professional guidance | Complex deferred tax calculations benefit from expert accounting and tax consulting support |

What is deferred tax and why does it matter?

Deferred tax represents the future tax consequences of transactions and events recognized in your current financial statements. When your accounting profit differs from your taxable profit, you create temporary differences that reverse over time. These differences arise because accounting standards and tax legislation treat certain items differently in terms of timing.

Your small business tax obligations require you to report taxable income to SARS based on tax rules, while your financial statements follow accounting standards. For example, you might recognize revenue in your accounts when you invoice a customer, but SARS only taxes that revenue when you receive payment. This timing gap creates a temporary difference requiring deferred tax recognition.

Temporary differences reverse in future periods, distinguishing them from permanent differences. Permanent differences never reverse and include items like entertainment expenses that accounting allows but tax disallows completely. Only temporary differences generate deferred tax.

Deferred tax assets arise when you will pay less tax in future periods. Common examples include provisions for doubtful debts that you recognize now but SARS only allows when debts become bad, or tax losses you can carry forward. Deferred tax liabilities occur when you will pay more tax later, such as when you claim accelerated depreciation for tax purposes but use straight line depreciation in your accounts.

Understanding deferred tax matters because it ensures your financial statements accurately reflect future tax obligations. Investors, lenders, and stakeholders rely on this information to assess your business’s true financial position. Misunderstanding deferred tax can lead to poor cash flow planning, inaccurate profit projections, and compliance issues with financial reporting standards.

Key temporary differences for South African SMEs:

- Depreciation timing between accounting and tax allowances

- Provisions recognized in accounts but not yet deductible for tax

- Revenue recognition differences between accrual and cash basis

- Prepaid expenses treated differently for accounting versus tax

- Employee benefit accruals not yet paid

Pro Tip: Review your financial statements quarterly to identify new temporary differences early. This proactive approach helps you anticipate future tax impacts and avoid surprises when filing returns.

How to identify and calculate deferred tax

Calculating deferred tax requires a systematic approach comparing the carrying amounts of assets and liabilities in your financial statements with their tax bases. The difference between accounting carrying amounts and tax bases creates deferred tax assets or liabilities that you must recognize.

Follow these steps to calculate deferred tax:

- Identify all assets and liabilities in your statement of financial position

- Determine the carrying amount of each item according to accounting standards

- Calculate the tax base of each item according to South African tax legislation

- Compute the temporary difference by subtracting tax base from carrying amount

- Classify differences as taxable or deductible temporary differences

- Apply the appropriate tax rate to each temporary difference

- Recognize deferred tax liabilities for taxable differences and assets for deductible differences

- Assess probability of future taxable profits to support deferred tax asset recognition

Taxable temporary differences lead to deferred tax liabilities because they will increase taxable amounts in future periods when the difference reverses. For instance, if you use accelerated depreciation for tax but straight line for accounting, your asset’s tax base becomes lower than its carrying amount. When you eventually dispose of the asset, you will have more taxable profit.

Deductible temporary differences create deferred tax assets because they will reduce taxable amounts in future periods. A provision for doubtful debts recognized in your accounts but not yet allowed by SARS creates a deductible difference. When the debt becomes bad and SARS allows the deduction, you will have less taxable profit.

Recognizing deferred tax assets requires careful judgment about future profitability. You can only recognize a deferred tax asset if you expect sufficient taxable profits in future periods to utilize the deduction. This requires realistic profit forecasting based on your business plans and market conditions.

| Item | Carrying Amount | Tax Base | Temporary Difference | Deferred Tax at 27% |

|---|---|---|---|---|

| Equipment | R100,000 | R70,000 | R30,000 taxable | R8,100 liability |

| Doubtful debt provision | R15,000 | R0 | R15,000 deductible | R4,050 asset |

| Prepaid insurance | R6,000 | R0 | R6,000 taxable | R1,620 liability |

| Accrued bonus | R20,000 | R0 | R20,000 deductible | R5,400 asset |

Pro Tip: Maintain a detailed schedule tracking temporary differences throughout the year. This working paper simplifies year end tax planning and ensures you capture all deferred tax items accurately.

Deferred tax under South African tax rules: important considerations

South African tax legislation significantly influences how you calculate and recognize deferred tax. The corporate income tax rate of 27% applies to most companies in 2026, and you must use this rate when measuring deferred tax unless a different rate will apply when the temporary difference reverses.

Capital gains tax adds complexity to deferred tax calculations. Companies include only 80% of capital gains in taxable income, creating an effective capital gains tax rate of 21.6% (27% × 80%). When temporary differences relate to assets that will generate capital gains on disposal, you must apply the lower effective rate to calculate deferred tax correctly.

South African corporate income tax rates and capital gains treatment require careful consideration when measuring deferred tax. Using the wrong rate leads to material misstatements in your financial statements and can trigger audit adjustments.

Common temporary differences in the South African context include wear and tear allowances versus accounting depreciation. SARS prescribes specific rates for different asset classes, often differing from the useful lives you determine for accounting purposes. This creates ongoing temporary differences requiring deferred tax recognition.

Provisions represent another frequent source of temporary differences. You might recognize a provision for warranties, legal claims, or environmental rehabilitation in your accounts, but SARS typically only allows deductions when you actually incur the expenditure. The timing gap creates deductible temporary differences and potential deferred tax assets.

South African specific deferred tax considerations:

- Apply the 27% corporate tax rate for most temporary differences

- Use the 21.6% effective rate for capital gains related differences

- Consider assessed losses and their expiry when recognizing deferred tax assets

- Account for timing of wear and tear allowances versus depreciation

- Review SARS guidelines on deductibility timing for provisions

Future taxable profits must be probable before recognizing deferred tax assets. SARS does not automatically accept all deferred tax asset claims, particularly for assessed losses carried forward. You need convincing evidence of future profitability, such as existing taxable temporary differences that will reverse, strong business forecasts, or a history of profitable operations.

| Scenario | Tax Treatment | Accounting Treatment | Deferred Tax Impact |

|---|---|---|---|

| Equipment depreciation | 20% wear and tear | 10% straight line | Deferred tax liability |

| Warranty provision | Deductible when paid | Recognized when sold | Deferred tax asset |

| Prepaid rent | Deductible when paid | Expensed over period | Deferred tax liability |

| Assessed loss | Carried forward | Recognized immediately | Deferred tax asset if probable |

Aligning your deferred tax calculations with SARS reporting requirements ensures consistency between your financial statements and tax returns. Discrepancies can trigger queries during audits or reviews. Your South African small business tax compliance improves significantly when deferred tax calculations accurately reflect SARS rules and timing requirements.

Pro Tip: Document your assessment of future taxable profits supporting deferred tax asset recognition. SARS and auditors often scrutinize these judgments, so maintaining clear evidence of your forecasting basis protects your position.

Managing deferred tax for effective financial planning and compliance

Proactive deferred tax management strengthens your financial planning and ensures compliance with reporting requirements. Identifying deferred tax issues early prevents last minute scrambles during financial statement preparation and tax filing deadlines.

Accurate bookkeeping forms the foundation of effective deferred tax management. You need detailed records of asset acquisitions, depreciation calculations, provision movements, and all transactions creating timing differences. Poor record keeping makes identifying temporary differences nearly impossible and increases the risk of errors.

Modern accounting software designed for South African businesses can automate much of the deferred tax tracking process. Cloud based platforms maintain parallel records for accounting and tax purposes, automatically flagging differences requiring deferred tax consideration. This technology reduces manual calculations and improves accuracy.

Cash flow planning must account for deferred tax movements even though deferred tax does not represent immediate cash payments. Changes in deferred tax balances affect your tax expense in the income statement, which influences reported profit and stakeholder perceptions. Understanding these impacts helps you communicate financial results more effectively.

Best practices for managing deferred tax:

- Implement robust systems tracking temporary differences throughout the year

- Reconcile accounting and tax records quarterly to identify new differences

- Document judgments about future profitability supporting deferred tax assets

- Review tax rate changes and their impact on existing deferred tax balances

- Engage qualified professionals for complex calculations or unusual transactions

- Train your finance team on deferred tax principles and identification

SMEs should invest in accounting software tools to identify and track deferred tax accurately to avoid costly mistakes. Manual spreadsheets become unwieldy as your business grows and temporary differences multiply. Purpose built software scales with your business and maintains the detailed audit trail required for compliance.

Common pitfalls include misclassifying permanent differences as temporary, overlooking small temporary differences that accumulate into material amounts, and failing to reassess deferred tax asset recognition as business circumstances change. Regular reviews with your accountant help catch these issues before they become problems.

Complex transactions such as business combinations, restructurings, or significant asset disposals create intricate deferred tax implications. Professional guidance becomes essential in these situations because errors can materially misstate your financial position. The cost of expert advice is minimal compared to the potential impact of getting deferred tax wrong.

Your year end tax planning process should include a comprehensive deferred tax review. This timing allows you to address any issues before finalizing financial statements and ensures your tax provision accurately reflects all temporary differences. Early identification of problems provides time to implement solutions.

Pro Tip: Schedule quarterly deferred tax reviews with your accountant rather than waiting until year end. This regular cadence catches issues early when they are easier to resolve and spreads the workload more evenly throughout the year.

How Ready Accounting can simplify your deferred tax management

Navigating deferred tax complexities becomes significantly easier with professional support tailored to South African SMEs. Ready Accounting offers cloud accounting solutions that automatically track temporary differences and calculate deferred tax balances in real time. Our systems maintain parallel accounting and tax records, eliminating manual reconciliation work and reducing error risk.

Our expert tax consulting services provide the specialized knowledge required for complex deferred tax scenarios. We help you assess future profitability for deferred tax asset recognition, apply the correct tax rates to different types of temporary differences, and ensure full compliance with South African financial reporting standards. Our team stays current with SARS rule changes affecting deferred tax calculations.

Cloud based accounting platforms deliver real time financial insights that transform how you manage deferred tax. You gain instant visibility into temporary differences as they arise, enabling proactive management rather than reactive corrections. This transparency supports better financial planning and more informed business decisions throughout the year.

Frequently asked questions about deferred tax

What is deferred tax?

Deferred tax is an accounting concept representing future tax consequences of temporary differences between accounting profit and taxable profit. It reflects timing differences in when you recognize income or expenses for financial reporting versus tax purposes. Deferred tax does not represent an immediate payment to SARS but ensures your financial statements accurately show future tax obligations or benefits.

How does deferred tax differ from current tax payable?

Current tax payable represents the actual amount you owe SARS for the current year based on taxable income. Deferred tax reflects timing differences that will affect future tax payments but involves no immediate cash outflow. Current tax appears as a liability you must pay, while deferred tax adjusts your financial statements to match tax expenses with the periods generating the underlying transactions.

When should I recognize a deferred tax asset?

Recognize a deferred tax asset only when you expect sufficient future taxable profits to utilize the deductible temporary difference. This requires realistic profit forecasting considering your business plans, market conditions, and historical performance. Reassess deferred tax asset recognition whenever circumstances change, as overstating these assets misleads stakeholders about your true financial position.

Does deferred tax affect my cash flow?

Deferred tax does not directly affect cash flow because it represents timing differences rather than actual payments. However, deferred tax movements impact your reported profit, which influences stakeholder perceptions and potentially affects financing decisions. Understanding deferred tax helps you explain profit fluctuations and communicate your true cash position more effectively to lenders and investors.

When should I seek professional help with deferred tax?

Seek professional assistance when facing complex transactions like business combinations, significant asset disposals, or restructurings. Also consult experts if you struggle to identify temporary differences, assess future profitability for asset recognition, or understand how South African tax rules apply to your specific situation. Professional guidance prevents costly errors and ensures compliance with financial reporting standards.

Recommended

- Small business tax in South Africa: essential 2026 guide – Ready Accounting

- Dividends tax in South Africa: essential guide for SMEs 2026 – Ready Accounting

- How to save tax in South Africa: smart strategies for SMEs in 2026 – Ready Accounting

- Year-End Tax Planning Guide for Small Businesses – Ready Accounting