Practical strategies to manage and reduce business debt

Executive Summary

- Business debt slowly accumulates and can cause severe financial strain if not managed carefully.

- Building a detailed debt map and practicing proactive credit management improves cash flow stability.

- External support and automation tools help SMEs control debt and protect growth opportunities.

Business debt has a way of creeping up quietly, then hitting hard. A single large unpaid invoice can set off a chain reaction that strains payroll, delays supplier payments, and forces you into expensive short-term borrowing. What makes this especially brutal is the math behind recovery: at a 10% profit margin, a single R1 bad debt requires R10 in new sales just to break even. For South African SMEs already navigating load shedding, rising input costs, and slow economic growth, that kind of pressure is not theoretical. It is existential. This guide cuts through the noise and gives you a practical framework to take control.

Table of Contents

- Understand your debt landscape

- Strengthen your credit management practices

- Optimize cash flow and reduce reliance on debt

- Leverage external support and government policy

- Why most debt advice misses the hidden costs

- Take control of your financial future

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Map your debt clearly | Accurately listing all debts and terms is the essential starting point for effective management. |

| Enforce strict credit policies | Careful client vetting and firm payment terms will drastically reduce future bad debt. |

| Optimize cash flow | Weekly monitoring, budgeting, and automation help keep your business resilient and minimize debt dependence. |

| Use available support | From government policies to expert advisors, external support can unlock new solutions and resources for debt management. |

| Mind hidden costs | The true cost of debt includes lost profits, wasted time, and missed opportunities—don’t underestimate these impacts. |

Understand your debt landscape

Before you can make progress, you need a clear view of where you stand. Most business owners carry a rough mental picture of what they owe and what they are owed, but rough pictures lead to rough decisions. You need precision.

Start by pulling together every debt obligation your business carries. This means bank loans, asset finance agreements, trade credit from suppliers, tax liabilities owed to SARS, and any director loans sitting on the balance sheet. For each item, record the creditor name, the outstanding balance, the interest rate, the monthly repayment amount, and the due date. Do the same exercise on the other side: every outstanding invoice from clients, the amounts, how old they are, and whether any payment arrangements are in place.

This gives you your first real debt map. A simple table works well for this:

| Creditor / Debtor | Type | Outstanding Amount | Interest Rate | Monthly Payment | Days Overdue |

|---|---|---|---|---|---|

| FNB Business Loan | Bank debt | R250,000 | 12.5% | R6,200 | Current |

| Supplier XYZ | Trade credit | R45,000 | 0% | R45,000 | 30 days |

| Client ABC Invoice | Receivable | R80,000 | N/A | N/A | 60 days |

| SARS VAT Account | Tax liability | R22,000 | 10.25% | TBC | 15 days |

Once you have built this table, look at your Days Sales Outstanding, or DSO. DSO measures how long it takes your business to collect payment after a sale. According to sector benchmarks in South Africa, construction businesses typically sit at 80 to 100 days, manufacturers at 45 to 70 days, and wholesale distributors between 30 and 55 days. The general rule is to keep your DSO below 1.5 times your standard payment terms. If your terms are 30 days and your DSO is 60, you have a structural problem that no amount of sales growth will fix.

Understanding cash flow problems and solutions is the logical next step once your debt map is in place, because cash flow and debt are always connected.

Beyond the obvious liabilities, watch for these red flags in your debt landscape:

- Overdue balances that have been “on hold” for more than 90 days without a written payment plan

- Suppliers who are extending less credit than they used to, which signals they are losing confidence in your ability to pay

- A growing gap between your bank balance and your profit on paper

- Recurring short-term borrowing to cover operating expenses rather than growth

- Tax submissions in arrears, which compound penalties quickly

These red flags do not always mean disaster, but they do mean you need to act now, not next quarter. Good expense management during slow periods can also buy you the breathing room to address these issues without making hasty decisions.

Strengthen your credit management practices

With a map of your current debt, it is time to prevent future problems. Credit management is not just an admin function. It is one of the most powerful levers you have for keeping the business financially healthy.

The foundation is vetting your clients before you extend credit. Many SMEs skip this step because they are hungry for revenue, but selling to a client who cannot or will not pay is worse than not making the sale at all. Here is a practical process to follow:

- Request a completed credit application from every new B2B client, including their trading name, registration number, bank details, and trade references.

- Verify the business through CIPC (Companies and Intellectual Property Commission) to confirm it is actively registered and in good standing.

- Run a credit bureau check through providers like TransUnion, Experian, or XDS to assess their payment history with other suppliers.

- Set a credit limit based on what their profile supports, not what they are asking for.

- Issue a formal credit agreement that spells out payment terms, interest on overdue balances, and your escalation process.

- Send automated reminders at 7, 14, and 30 days before and after the due date.

- Escalate to collections if the account reaches 90 to 120 days overdue, as recommended best practice for South African B2B businesses.

The contrast between proactive and reactive credit management is stark. Reactive businesses chase invoices after they are already overdue and often write off debt they should have recovered. Proactive businesses have systems that make late payment uncomfortable for the client from day one.

| Approach | Action taken | Typical outcome |

|---|---|---|

| Reactive | Chases overdue invoices manually | High write-off rates, strained client relationships |

| Proactive | Automated reminders, credit vetting, clear escalation | Lower DSO, fewer write-offs, predictable cash flow |

Understanding your director responsibilities as an SME leader matters here too, because allowing bad debts to accumulate unchecked can create personal liability in certain circumstances.

Pro Tip: Do not wait for an invoice to become overdue before making contact. A quick, friendly call or email five days before the due date dramatically increases on-time payment rates. It signals professionalism and reminds the client without creating awkwardness.

Optimize cash flow and reduce reliance on debt

Preventing debt is easier when cash flow is healthy. Most SMEs reach for debt when cash runs short, but the better question is why the cash ran short in the first place. Addressing the root cause reduces your need to borrow at all.

![]()

The starting point is a rolling cash flow forecast. This is not a once-a-year budget exercise. It is a living document, updated weekly, that shows your expected inflows and outflows for the next 8 to 13 weeks. When you can see a cash gap forming three weeks out, you have options. When you see it the day before payroll, you have a crisis.

A striking statistic from Business Partners illustrates how widespread this problem is: 72% of South African SMEs have drawn on personal savings to cover business cash flow shortfalls. That is not a business strategy. That is a survival reaction, and it puts both your personal and business financial security at risk simultaneously.

To break that cycle, focus on these practical improvements:

- Invoice immediately after delivering goods or services. Every day you delay is a day added to your collection timeline.

- Offer early payment incentives such as a 2% discount for payment within 7 days. The discount costs less than overdraft interest.

- Negotiate extended terms with suppliers where possible, while shortening the terms you offer clients.

- Use cloud-based accounting software like Xero or Sage to track receivables and payables in real time, not from a spreadsheet updated once a month.

- Set up automated debit orders or payment links so clients can pay instantly without needing to log into internet banking.

- Separate your operating account from a buffer account, keeping one to two months of fixed costs in the buffer to absorb seasonal fluctuations.

The link between automation and cash flow is not a future concept. Businesses using automated billing and reconciliation collect faster and have far fewer errors in their debtor records. That accuracy matters when you need to make fast decisions about where to allocate resources.

Pro Tip: Schedule a fixed 30-minute weekly cash flow review every Monday morning. Treat it like a standing meeting with your most important stakeholder: your bank balance. Reviewing it weekly means small problems get caught before they become large ones.

Leverage external support and government policy

Even with the right practices, external support can make a vital difference. Managing business debt alone, especially when it has already grown complex, is both stressful and expensive in terms of mistakes made.

South Africa’s government has specific programs aimed at improving SME access to finance and debt management tools. The MSMEs Funding Policy promotes a Fund of Funds model, credit guarantee schemes, and the use of alternative credit data to give smaller businesses better access to formal financing. This means that even if your traditional credit score is weak, there are pathways to funding that do not require you to mortgage your home.

Here is how to engage this ecosystem effectively:

- Contact the Small Enterprise Development Agency (SEDA) for free business advisory services and referrals to appropriate funding programs.

- Approach the National Empowerment Fund (NEF) or SEFA if your business qualifies for targeted funding support based on ownership or sector.

- Engage a registered debt counsellor or business rescue practitioner if your debt has reached a level where normal repayment is not feasible. Early intervention here is critical.

- Work with your bank’s relationship manager, not just the call centre, to negotiate restructured repayment terms before you miss a payment.

- Consult a Fractional CFO or accounting firm with SME experience to run a full debt impact analysis and build a structured repayment plan.

“Businesses that engage professional advisors before reaching a crisis point consistently achieve better debt restructuring outcomes than those that wait until they are already in default. The cost of advice is almost always less than the cost of the mistake it prevents.”

The role of alternative credit information is growing in South Africa. If your bank uses only traditional credit bureau data to assess you, platforms and lenders using utility payment history, supplier payment records, and cash flow data may offer better terms. This is worth exploring before accepting a high-interest emergency facility.

Strong financial planning for your SMB is what allows you to engage external support from a position of knowledge rather than desperation. When you walk into any funding conversation with accurate financials, a clear repayment plan, and a realistic cash flow forecast, your credibility increases dramatically.

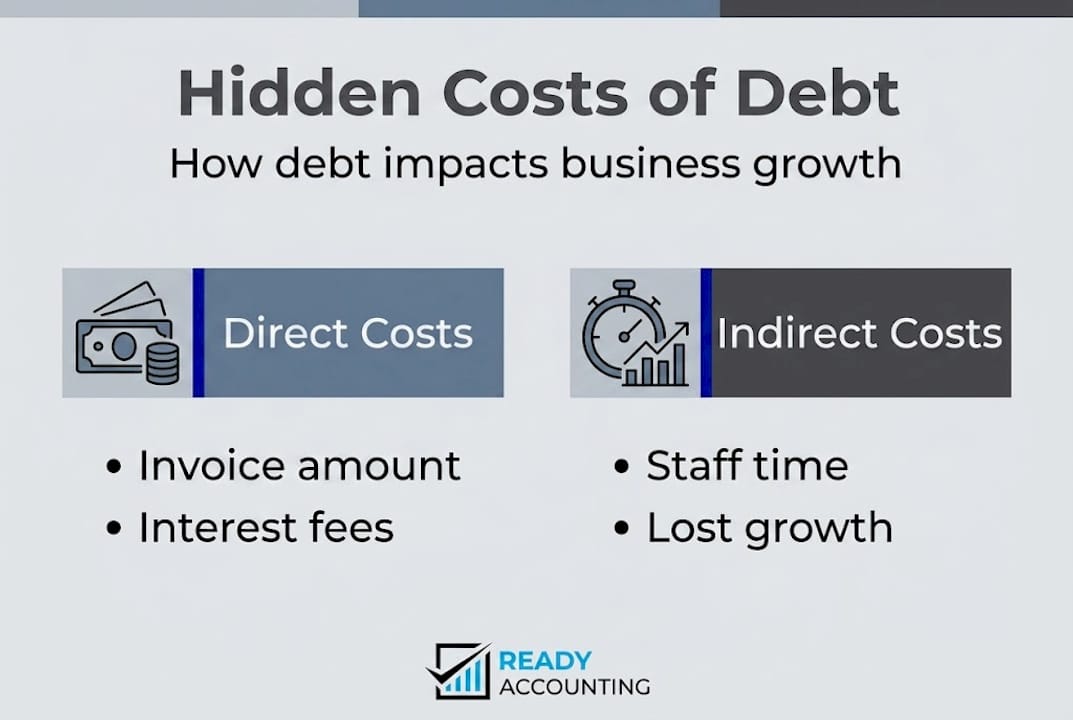

Why most debt advice misses the hidden costs

You have seen the step-by-step strategies. Now let us address something that most articles and advisors completely ignore.

When business owners think about bad debt, they think about the face value of what is owed. A client owes you R50,000. You write it off. That is the loss. Except it is not. The real costs of bad debt extend far beyond the invoice amount into territory most people never calculate.

Consider what actually happens when you chase a large overdue invoice for three months. Your senior staff spend hours making calls, writing emails, and attending difficult conversations. You delay decisions about hiring or equipment because the cash you expected has not arrived. You borrow at high rates to cover the gap. You lose a client anyway. You write off not just the R50,000 but also the VAT you already paid to SARS on that invoice. And you end up with a team that is demoralized from the distraction.

That is not a R50,000 loss. It is a R80,000 to R100,000 loss in real terms, plus the growth you did not pursue while you were dealing with it.

The mindset shift that changes results is treating credit management as a growth function, not a compliance function. When you protect your receivables aggressively, you are not being difficult. You are protecting your capacity to grow, pay your team, and invest in the business.

Pro Tip: Before writing off any debt, run a full impact analysis that includes staff time spent, borrowing costs incurred, VAT exposure, and opportunity cost. The number will almost always shock you and motivate better upfront credit decisions. Also consider the tax implications of writing off bad debt, as there are specific SARS rules around bad debt deductions that you must follow correctly.

Take control of your financial future

The strategies in this article only deliver results when they are actually implemented consistently, and that is where most SMEs struggle. The discipline required to maintain weekly cash flow reviews, enforce credit policies with valued clients, and keep your debt map updated is real. It is also exactly where the right financial infrastructure makes the difference.

At Ready Accounting, we build cloud-based financial systems that automate the monitoring, reporting, and alerting that keeps your debt under control without adding hours to your week. From real-time dashboards that flag overdue receivables to automation for better cash flow management, our approach turns your finance function into a proactive tool rather than a reactive headache. If you want to understand how automation fits into your broader financial strategy, our guide to accounting automation is the right place to start.

Frequently asked questions

What is the first step to managing business debt effectively?

List all outstanding debts including amounts, payment terms, and creditors to build a complete picture before taking any action. You cannot prioritize what you have not measured.

How can I reduce dependence on personal savings for my business?

Implement automated cash flow monitoring, strict budgeting, and seek professional advice early to prevent the cash crunches that force 72% of SA SMEs to dip into personal funds.

When should I hand over overdue debts to a collection agency?

South African best practice is to hand over accounts between 90 and 120 days overdue, as recovery rates drop significantly beyond that window.

What government support exists for South African SMEs struggling with debt?

The MSMEs Funding Policy offers credit guarantees, alternative credit data programs, and a Fund of Funds model specifically designed to improve access to finance for smaller businesses.

What is the danger of ignoring overdue receivables?

Overdue receivables erode profit faster than most owners realize: at a 10% margin, every R1 lost to bad debt requires R10 in new revenue to replace, making early intervention far cheaper than delay.