How to read an income statement for smarter decisions

Executive Summary

- The income statement reveals a business’s profitability, distinct from cash flow, which is critical for decision-making.

- Proper analysis of key margins and line items helps SME owners identify operational issues early and improve financial health.

- Compliance with IFRS for SMEs and regular review of financials support tax, funding, and growth strategies.

Many South African SME owners feel a quiet sense of dread when their accountant sends over the monthly financials. The income statement sits at the centre of that anxiety, packed with line items, subtotals, and percentages that can feel more like a foreign language than a business tool. Yet this single document holds the clearest picture of whether your business is actually making money, bleeding cash, or somewhere in between. Read it correctly, and you gain a genuine competitive edge. Ignore it, and you are flying blind in one of the most demanding business environments in the world.

Table of Contents

- What is an income statement and why does it matter?

- Key line items explained: your income statement from top to bottom

- Regulatory standards for SME income statements in South Africa

- How to analyse and use your income statement for better decisions

- Why most SME owners misuse their income statement (and what to do instead)

- Put your insights into action with automated accounting solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Understand key sections | Income statements show your revenues, expenses, and profits from top to bottom for a given period. |

| Use analysis techniques | Apply vertical, horizontal, and margin analysis to identify trends and spots issues early. |

| Follow SA regulations | Ensure your income statement complies with IFRS for SMEs and SARS rules for accurate reporting. |

| Focus on margins | Track gross and operating margins for core business health instead of only watching net profit. |

| Leverage automation | Automated solutions can simplify your reporting and help catch problems before they affect profits. |

What is an income statement and why does it matter?

An income statement summarises revenues, expenses, and profitability over a specific period, flowing from top-line revenue down to bottom-line net income. You may also hear it called a profit and loss statement, or simply a P&L. Both terms refer to the same report, though “income statement” is the more formal, standards-compliant name used in audited accounts.

The income statement does not show you cash in the bank. It shows you whether the business activity itself is profitable. Cash flow and profit are two very different things.

This distinction matters enormously for South African SMEs. A business can show a healthy net profit on paper while simultaneously struggling to pay suppliers, simply because clients have not settled their invoices yet. Understanding that boundary between profitability and liquidity is your first step toward smarter financial management.

The report covers a defined period, typically a month, a quarter, or a financial year. It answers one core question: did the business earn more than it spent during that time? From that foundation, you can build trend analysis, cash flow forecasts, and pricing strategies.

There are two common formats. A single-step income statement groups all revenues together and all expenses together, then subtracts one from the other for a single profit figure. It is simple but limited. A multi-step income statement breaks the journey into stages, showing gross profit, then operating profit, then net profit. Most growing South African SMEs benefit from the multi-step format because it reveals where value is created and where it leaks away.

Our financial statements guide covers how the income statement fits alongside your balance sheet and cash flow statement, the three pillars of complete financial visibility.

Key reasons why South African SME owners must master this report:

- SARS compliance requires accurate revenue and expense records for tax returns

- Funding applications to banks or investors always request recent P&L statements

- Operational decisions on staffing, pricing, and cost control depend on margin data

- Early warning signals of declining profitability appear here before they hit your bank account

Key line items explained: your income statement from top to bottom

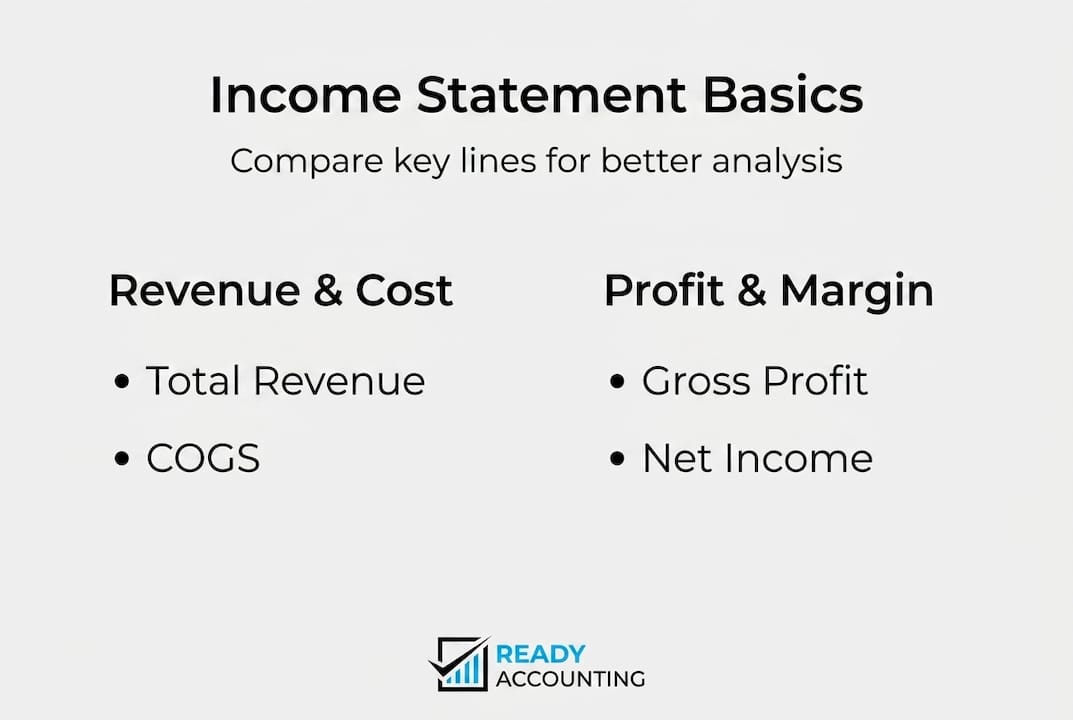

Key line items include revenue at the top, then Cost of Goods Sold (COGS), Gross Profit, Operating Expenses, Operating Income (EBIT), interest and taxes, and finally Net Income at the bottom. Each layer strips away another cost to show you a purer view of performance.

Here is how to read each section:

-

Revenue (turnover): The total sales your business generated before any costs. For a Cape Town clothing retailer, this is every rand collected from customers. Watch for returns, discounts, and allowances, which are deducted to arrive at net revenue.

-

Cost of goods sold (COGS): The direct costs tied to producing or delivering your product or service. For a manufacturer, this includes raw materials and factory labour. For a logistics company, it is fuel and driver wages. COGS does not include your office rent or your own salary.

-

Gross profit: Revenue minus COGS. This tells you how much money remains after covering the cost of what you actually sold. Your gross profit margins show the efficiency of your core operations, independent of overhead.

-

Operating expenses (OpEx): Costs that keep the business running but are not tied to individual units of output. Think salaries for admin staff, marketing spend, software subscriptions, and office rental.

-

Operating income (EBIT): Earnings Before Interest and Tax. This is gross profit minus operating expenses. It reflects the profitability of your core business model, stripped of financing costs and tax.

-

Interest and taxes: Loan interest payments and your income tax liability are separated here so you can see their individual impact on the final result.

-

Net income (bottom line): What remains after every single cost. This is the number most owners obsess over, though as you will see in the perspective section, it can mislead you if taken in isolation.

| Line item | Formula | What it reveals |

|---|---|---|

| Gross profit | Revenue minus COGS | Core production efficiency |

| Operating income | Gross profit minus OpEx | Business model strength |

| Net income | Operating income minus interest and taxes | Overall period profitability |

| Gross margin % | Gross profit divided by revenue | Pricing and cost control |

| Net margin % | Net income divided by revenue | Total bottom-line efficiency |

Pro Tip: Calculate your gross margin percentage every single month, not just at year end. A margin dropping by more than 3 percentage points month on month is an early warning sign worth investigating immediately, before it becomes a crisis.

For a deeper look at each section with South African business examples, the income statement details resource walks through real-world scenarios.

Regulatory standards for SME income statements in South Africa

Once you know the line items, it is critical to understand how South African law and accounting standards shape the structure and content of your statement.

South African SMEs follow IFRS for SMEs, a simplified version of International Financial Reporting Standards that covers the statement of comprehensive income, including revenue recognition and tax treatment per SARS rules. This is not optional. If your business prepares financial statements for a bank, investor, or compliance purpose, IFRS for SMEs sets the minimum standard.

What does this mean practically? Your income statement must:

- Recognise revenue only when it is earned, not when cash is received (accrual accounting)

- Separate operating income from financing costs and tax clearly

- Disclose any unusual or non-recurring items separately

- Apply consistent accounting policies year on year

The SARS dimension adds another layer. Your taxable income is calculated from your accounting profit, with specific adjustments. Items like depreciation are replaced by SARS capital allowances. Entertainment expenses are often partially disallowed. Knowing these adjustments prevents nasty surprises at assessment time. More detail on this is covered in our SA SME tax returns guide.

| Format | Best for | Key advantage |

|---|---|---|

| Single-step | Very small sole traders | Simple and quick to prepare |

| Multi-step | Growing SMEs, investor-ready businesses | Shows gross and operating profit separately |

| IFRS for SMEs | Any SME with external stakeholders | Internationally recognised, SARS-aligned |

South African SME benchmarks paint a sobering picture. The average after-tax profit margin across SA businesses sits at just 1.3%, with manufacturing at 1.5% and trade businesses at 1.0%. Load-shedding costs, currency volatility, and rising input prices all compress margins. Knowing where your numbers sit relative to your sector helps you set realistic targets.

Pro Tip: Request sector-specific benchmarks from your accountant or industry association annually. Comparing your gross margin to the industry average reveals whether your pricing and cost structure are competitive, or whether you are absorbing costs your competitors are not.

For practical templates and worked examples, our SA SME financial statement examples and financial statement basics pages are useful starting points.

How to analyse and use your income statement for better decisions

With legal and technical requirements clear, let us move from understanding to practical application. How do you actually use your income statement to manage and grow your business?

There are two core analysis methods every SME owner should know. Vertical analysis expresses every line item as a percentage of revenue, while horizontal analysis tracks the same line items across multiple periods to reveal trends. For SMEs, reviewing monthly or quarterly catches problems before they escalate. Use both together for the most complete picture.

Here is a practical process you can follow each month:

-

Run vertical analysis first. Divide every major cost line by total revenue. If COGS is 55% of revenue this month versus 48% last month, something has changed in your production costs or pricing. Investigate before moving on.

-

Compare to the prior period. A 10% or greater month-on-month change in any major line item deserves attention. Revenue growth is good. But if operating expenses grow faster than revenue, your margins are shrinking even if profit looks fine in absolute terms.

-

Calculate your three key margins. Gross margin, operating margin, and net margin. Track them on a simple spreadsheet. Trends matter more than single data points.

-

Benchmark against your sector. Use Stats SA data, industry associations, or your accountant’s client base as reference points. If your gross margin is 12% and your industry average is 22%, the gap is telling you something specific about pricing or cost structure.

-

Connect the income statement to your cash flow. Profit does not equal cash. Your cashflow forecasting process should start with net income and then adjust for timing differences like debtor days and creditor payment terms.

Key actions to take when your income statement analysis flags a problem:

- Rising COGS: Renegotiate supplier terms, review waste in production, or adjust pricing to protect gross margin

- Bloated OpEx: Audit every recurring cost line. Subscriptions, insurance, and staffing costs often creep up unnoticed

- Shrinking net margin: Check if interest costs have increased due to new debt, or if once-off costs are distorting the picture

- Stagnant revenue: Combine income statement data with customer data to identify which product lines or client segments are driving or dragging performance

The income statement is most powerful when it is not read in isolation. Pair it with your balance sheet to understand asset efficiency, and with your cash flow statement to understand liquidity. Together, these three reports give you a complete picture of business health.

Why most SME owners misuse their income statement (and what to do instead)

Here is an uncomfortable truth we see repeatedly in our work with South African SMEs: most owners look at net profit, feel relieved or alarmed, and then close the report. That single number is often the least reliable signal on the page.

Net income is vulnerable to distortion. A once-off asset sale, an insurance payout, or a large once-off expense can swing it dramatically in either direction without reflecting any change in core business performance. Gross and operating margins are far more reliable indicators of core health. Strip out non-recurring items before drawing any conclusions about trends.

The South African context amplifies this problem. Load-shedding adds irregular generator and UPS costs. Currency swings affect import costs unpredictably. Debtor days stretch in a tight economy, creating timing mismatches between reported profit and actual cash. SARS compliance costs appear as once-off expenses in some periods and recurring ones in others. All of these make a naive reading of net profit genuinely misleading.

The fix is not complicated, but it requires discipline. Focus on whether your gross margin trend is stable or improving. That single metric, tracked consistently across 12 months, will tell you more about the underlying health of your business than any single month’s net profit figure. Look at real SME statement examples to see how this plays out in practice across different sectors and business sizes.

The businesses we see scale successfully are not the ones with the highest single-month profit. They are the ones that understand their margin structure deeply enough to make pricing, staffing, and investment decisions with confidence, even in volatile conditions.

Put your insights into action with automated accounting solutions

Applying new income statement skills in your daily operations becomes much easier with smart tools on your side. Manual bookkeeping introduces errors that corrupt the very data you are trying to analyse, and in a SARS environment that is increasingly algorithmically driven, those errors carry real financial risk.

Ready Accounting builds custom cloud accounting infrastructure for South African SMEs that automates income statement generation, margin tracking, and compliance reporting in real time. You get dashboards that flag margin shifts the moment they happen, not weeks later when the damage is done. Explore how automation improves cash flow, read our guide to accounting automation, or see how we approach improving financial reporting for growing businesses. Your income statement should work for you, not against you.

Frequently asked questions

What is the difference between a single-step and a multi-step income statement?

A single-step statement groups all revenues and all expenses into two buckets, while a multi-step statement shows detailed subtotals like gross profit and operating profit, making it far more useful for business analysis and investor reporting.

How often should I review my SME’s income statement?

South African SME owners should review monthly or quarterly to catch financial issues early and stay on track with budgets, rather than waiting for the annual financial statements.

What is a healthy profit margin for a South African SME?

The average after-tax margin across SA businesses is currently 1.3%, with manufacturing at 1.5% and trade at 1.0%, though healthy margins vary significantly by sector and business model.

Which line item should I focus on to improve my business quickly?

Focus on gross profit margin and operating expenses, as gross and operating margins reflect core business health more reliably than net income and are more directly within your control on a day-to-day basis.

How does income statement analysis help with SARS compliance?

An accurate income statement ensures all revenues and expenses are correctly recorded under IFRS for SMEs standards, which directly supports correct tax filings and reduces the risk of SARS penalties or audit triggers.