How to detect financial fraud in your South African SME

Executive Summary

- South African SMEs are vulnerable to simple, prevalent fraud schemes like under-declaration of income and false deductions.

- Basic controls such as segregation of duties, regular reconciliations, and approval processes effectively prevent fraud.

- Routine checks like bank feed reviews and staff tips are more effective for SMEs than advanced AI tools.

Financial fraud is not a distant threat for South African small business owners. It is happening right now, in businesses much like yours, and most owners only find out after the damage is done. SARS investigative audits on SMEs generated R8.3 billion in additional revenue in 2017/18 alone, which tells you exactly how seriously the taxman takes non-compliance at the SME level. This guide walks you through the most common fraud types targeting South African businesses, the tools and controls you need to monitor for them, and a clear step-by-step detection process you can start using immediately.

Table of Contents

- Common types of financial fraud in South African SMEs

- What you need to detect fraud: Tools, controls, and compliance basics

- Step-by-step fraud detection process for South African SMEs

- What to do if you find (or suspect) fraud

- Why simple, regular checks beat advanced AI for most South African SMEs

- Get expert support to keep your business fraud-free

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know the risks | SMEs are heavily targeted for tax and financial fraud, making prevention crucial. |

| Set up strong controls | Basic internal checks work better for most SMEs than complex tools alone. |

| Detect fraud step by step | Use clear processes and multiple red flags, not just financial ratios. |

| Act fast if fraud found | Secure evidence and report using SARS and legal protocols to reduce risk. |

| Stay compliant | Keep records for five years and regularly update your finance practices. |

Common types of financial fraud in South African SMEs

South African SMEs face a specific and growing range of fraud risks. Some are internal, driven by employees or management. Others are external, carried out by suppliers, customers, or cybercriminals. Most business owners are not caught off guard by complex schemes. They are caught off guard by simple ones that were hiding in plain sight.

The most widespread fraud types you need to recognise include:

- Under-declaration of income: Deliberately recording less revenue than was actually earned to reduce taxable income. This is especially common in cash-intensive businesses like restaurants, retail, and service trades.

- False deductions: Claiming personal expenses as business costs, inflating legitimate expenses, or fabricating receipts entirely.

- Phony or duplicate invoices: A supplier (or a dishonest employee) submits invoices for goods or services never delivered. Duplicate invoice schemes are particularly easy to run in businesses without tight approval processes.

- Payroll fraud: Ghost employees on the payroll, inflated salaries for connected parties, or manipulation of leave and overtime records.

- Digital banking fraud: Business email compromise (BEC), where fraudsters impersonate suppliers and redirect payments to their own accounts. South Africa has one of the highest rates of cybercrime exposure in Africa, making this a growing threat.

Important: SARS tax fraud specifically includes under-declaration of income and false deductions. These are not just internal business risks. They are criminal acts that SARS actively investigates and prosecutes.

Cash-intensive operations attract particular attention from SARS because the paper trail is thin and the temptation to under-report is higher. If your business handles significant cash, you are statistically more likely to face a lifestyle audit, where SARS compares your personal assets and spending against your declared income. Emerging fraud warning signs include subtle shifts in employee behaviour, unexpected changes in supplier payment patterns, and unusual spikes in specific expense categories.

Learning to spot these patterns early is what forensic accounting protection is built around. But before you can call in specialists, you need your own basic monitoring in place.

What you need to detect fraud: Tools, controls, and compliance basics

Now that you know the threats, here is what you need in place before you can monitor for them effectively.

Most fraud in SMEs succeeds not because of sophisticated schemes but because of weak controls. Three foundational controls every South African SME needs are segregation of duties, regular reconciliations, and formal approval processes. Segregation of duties means no single person can initiate, approve, and record a transaction. Reconciliations catch discrepancies between what your books say and what actually happened. Approval processes create accountability and a paper trail.

Understanding the Fraud Triangle also helps. The Fraud Triangle model identifies three conditions that make fraud likely: pressure (financial stress, personal problems), opportunity (weak controls, single points of access), and rationalisation (the fraudster justifies the act). When you can see these three elements converging around a person or process, your fraud risk is elevated. Monitoring for these human factors alongside your financial data dramatically improves early detection.

Here is a practical reference table for records you must maintain for both SARS compliance and fraud monitoring:

| Record type | Why it matters | Review frequency |

|---|---|---|

| Bank statements | Verify actual cash flows against recorded transactions | Monthly |

| Supplier invoices | Detect phantom or duplicate billing | Per transaction, reconcile monthly |

| Payroll records | Confirm employees and amounts are legitimate | Every pay run |

| VAT invoices | Ensure input/output VAT claims are supported | Monthly/quarterly |

| Expense receipts | Validate all deductions claimed | Monthly |

| General ledger | Catch unusual entries or adjustments | Monthly |

Your technology setup matters too. SARS eFiling is not optional; it is your primary compliance channel. Beyond that, secure cloud accounting platforms like Xero or QuickBooks provide real-time visibility into your financials. Pair these with strong access controls: unique logins per user, two-factor authentication, and role-based permissions so staff only see what they need to.

Getting the financial controls basics right first is what makes everything else in this guide work. A solid tax compliance guide will also show you the specific SARS requirements that sit alongside your fraud prevention work.

Pro Tip: Even a simple daily bank feed review in your accounting software, which takes about ten minutes, will flag discrepancies before SARS does. Most business owners who discover fraud early do so through a routine review, not a forensic investigation.

For more advanced digital environments, a digital fraud management guide provides a broader framework for securing payment processes and communication channels.

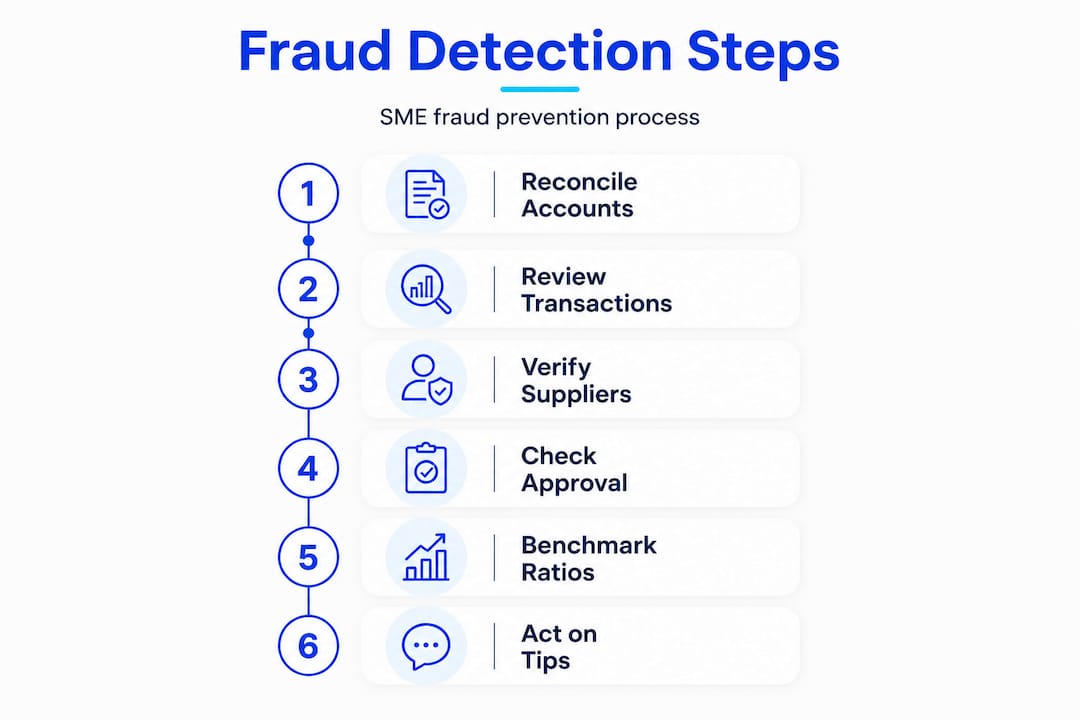

Step-by-step fraud detection process for South African SMEs

With tools and compliance basics in place, here is exactly how to detect fraud, step by step.

Step 1: Reconcile your bank accounts monthly. Compare every transaction in your accounting software to your actual bank statement. Unexplained differences, even small ones, need a written explanation. Fraudsters often start small to test whether anyone is watching.

Step 2: Review and categorise all unusual transactions. Look for round-number payments (R5,000 exactly, for example), payments to new suppliers not on your approved list, and any payment made outside your normal business hours. These are classic red flags. Understanding how to properly audit financial statements gives you a baseline for what normal looks like.

Step 3: Verify all active suppliers and customers. Confirm that every supplier invoicing you is a real, registered entity with a valid tax number. Check their banking details against what you have on file. BEC scams typically work by changing a legitimate supplier’s account number in your system. Call the supplier directly on a number you already know before making any large payment to updated banking details.

Step 4: Review approval processes and audit trails. Check that every payment above a set threshold (you define this, but R10,000 is a common starting point) has a proper approval chain. Look at who approved what, and when. Fraudulent transactions often slip through because someone bypassed an approval step. The detailed steps in how to audit financial records are particularly useful here.

Step 5: Check financial ratios and benchmark against your industry. Look at your expense ratios, particularly how your cost of sales and operating expenses trend as a percentage of revenue. The Fraud Triangle model shows strong correlation between fraud risk and markers like high accruals, poor liquidity, and high leverage. These ratios shift when fraud is present, but not always in obvious ways.

Step 6: Act on staff tip-offs and behavioural changes. The majority of fraud is first spotted by colleagues, not systems. Create a confidential tip-off mechanism. Watch for employees who never take leave (they may be covering ongoing fraud), lifestyle changes that seem inconsistent with their salary, or defensiveness about their work being checked.

Here is a comparison of detection methods so you can allocate your attention correctly:

| Method | Cost | Skill required | Most effective for |

|---|---|---|---|

| Bank feed review | Free | Low | Payment fraud, duplicate payments |

| Staff tip-off channel | Low | Low | Internal collusion, payroll fraud |

| Supplier verification calls | Free | Low | BEC, phony invoices |

| Financial ratio analysis | Low | Medium | Trend-based anomalies |

| Forensic accounting | High | Expert | Complex or confirmed fraud |

| Machine learning tools | High | Expert | High-volume transaction fraud |

It is worth noting that financial ratio analysis has limited effectiveness on its own, because sophisticated fraudsters conceal their activities by adjusting multiple accounts simultaneously. This is why you need to use multiple methods together, not rely on any single signal.

Fraud detection technology using machine learning is powerful in high-volume environments, but most SMEs get a better return by strengthening human checks and basic reconciliation processes first.

Pro Tip: Document every step you take during a fraud check. If SARS ever audits you, your internal monitoring records demonstrate good faith, reduce penalties, and show that any discrepancies were caught and corrected proactively.

What to do if you find (or suspect) fraud

After following the detection steps, be prepared to act immediately if you discover anything suspicious. Speed matters. Delayed action allows evidence to be destroyed and funds to disappear.

Here is the process to follow:

-

Secure all evidence first. Back up relevant financial records, emails, and documents before anyone can alter or delete them. Do not confront the suspected fraudster before you have done this.

-

Separate the involved staff member. If internal fraud is suspected, remove the employee’s access to financial systems immediately. Reassign their duties temporarily. Do this quietly and professionally to avoid tipping them off before a formal investigation begins.

-

Consult a forensic accountant or legal professional. A forensic accountant can quantify the loss, identify how the fraud was committed, and prepare evidence that holds up legally. Legal counsel ensures your response does not inadvertently expose you to unfair dismissal claims or other liability.

-

Determine if SARS reporting is required. If the fraud involved under-declaration of income or false VAT claims, you may have a tax liability exposure. SARS offers a Voluntary Disclosure Programme (VDP) that allows businesses to correct tax errors before SARS discovers them. Using the VDP reduces penalties significantly and demonstrates good faith.

-

File FICA reports where applicable. Under the Financial Intelligence Centre Act, certain suspicious transactions must be reported. Your accountant or legal advisor can confirm whether your situation triggers a reporting obligation.

-

Implement corrective controls immediately. Once the incident is contained, close the gap that allowed the fraud to happen. Update approval processes, change access credentials, and communicate the policy change to staff without singling out any individual.

Critical: Maintain five years of financial records at minimum. SARS can request records going back that far during any audit, and your fraud investigation documentation should be retained for the same period.

Proper reporting of financial irregularities protects you legally and limits your exposure. Detailed fraud reporting procedures also provide a structured template you can adapt for your business context.

Why simple, regular checks beat advanced AI for most South African SMEs

There is a persistent myth in the business world that only the most sophisticated technology can protect you from fraud. The idea that machine learning algorithms with 96 to 99 percent accuracy benchmarks are what stand between your business and financial crime is compelling, but largely irrelevant for most South African SMEs.

Here is the honest truth from working with scaling South African businesses: the fraud that actually hurts SMEs almost never requires a machine learning model to detect. It requires someone to look at the bank statement. The vast majority of internal fraud cases we see could have been caught weeks or months earlier if the business owner had simply done a ten-minute bank feed review each week. The fraudster was not using sophisticated concealment techniques. They were relying on the fact that nobody was looking.

Advanced tools absolutely have their place. For fintech companies, high-volume e-commerce businesses, or businesses with complex multi-entity structures, ML-powered fraud detection is worth the investment. But for a business turning over R5 million to R50 million a year, the highest-return fraud prevention investment is a clear approval process, a monthly reconciliation, and a culture where staff know that controls are real and enforced consistently.

The best practices in financial management for South African SMEs consistently show the same pattern: the businesses with the fewest fraud losses are not the ones with the fanciest software. They are the ones where the owner or a trusted manager looks at the numbers every week without fail. Consistency beats complexity every time.

This does not mean ignoring technology. It means being strategic about it. Automate your reconciliations so they happen faster. Use cloud accounting so you have real-time visibility. Enable bank feed integrations. These are practical, affordable upgrades that put simple controls on autopilot. Save your budget for expert forensic support when you actually need it, not for AI dashboards that generate alerts nobody has time to investigate.

Get expert support to keep your business fraud-free

If you have read this far and you are thinking about the gaps in your current controls, that instinct is worth acting on. At Ready Accounting, we help scaling South African SMEs and startups replace manual, fragile processes with cloud-based financial infrastructure that catches discrepancies before they become crises. From setting up real-time dashboards that flag unusual transactions to structuring your records so you are always SARS audit-ready, we treat your finance department as a strategic asset. Explore how automation improves cash flow visibility, see what better financial reporting looks like in practice, and learn how to reduce your SME tax liability while staying fully compliant.

Frequently asked questions

What are the most common financial fraud schemes targeting SA SMEs?

The most common include under-declaring income and false deductions, as well as fake supplier invoices, payroll manipulation, and digital banking fraud like business email compromise.

What triggers a SARS audit for small businesses?

SARS investigative audits are commonly triggered by inconsistent income declarations, high cash turnover with low declared profit, or expenses that are significantly above industry norms for your sector and size.

How long must SMEs keep records to stay compliant?

At least five years for all tax records, including invoices, bank statements, payroll records, and any supporting documentation for deductions claimed.

Do advanced analytics tools work for SME fraud, or are simpler methods better?

While ML tools achieve high accuracy benchmarks in enterprise environments, most SMEs get a far better return from consistent bank reconciliations, clear approval processes, and regular management review of their numbers.

What should I do if I discover fraud in my business?

Immediately secure all evidence, remove the involved party’s system access, consult a forensic accountant or legal advisor, and if tax fraud is involved, consider using SARS’s VDP to correct your position before SARS identifies the discrepancy independently.