South Africa business entity guide for smart owners

Executive Summary

- Choosing the right business structure in South Africa impacts liability, tax obligations, and compliance from startup to growth. While sole proprietorships and partnerships offer simplicity, registered companies like private or non-profit entities provide limited liability and better long-term scalability. Regular review and expert support are essential to adapt your business entity as your enterprise evolves and expands.

Picking a business structure feels like a once-off admin task, but it shapes every tax bill, personal liability risk, and compliance obligation your business will ever face. SARS makes it clear that the mechanics of entity selection hinge on two critical questions: do you need a separate legal personality with limited liability, or are you comfortable with personal exposure? And does your chosen structure trigger specific SARS registration and ongoing compliance obligations? The wrong answer to either question can cost you far more than any registration fee ever would.

Table of Contents

- Overview of business entities in South Africa

- Comparing liability and tax for each entity type

- Registration, SARS compliance, and tax incentives

- When to choose which entity: Practical considerations

- The uncomfortable truth about business structures in South Africa

- How expert support can simplify structuring and compliance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Entity choice impacts liability | Your decision on business structure determines how protected your personal assets are from company debts. |

| Tax obligations differ by structure | Sole proprietors and partnerships are taxed on personal returns, while companies are taxed separately. |

| No new close corporations | You cannot register a new close corporation in South Africa, so consider company structures for new businesses. |

| Register with SARS promptly | You must register as a taxpayer with SARS within 21 days of starting any business activities. |

| Review your structure as you grow | Revisit your choice of entity regularly to ensure it fits your expanding business and compliance needs. |

Overview of business entities in South Africa

South Africa’s legal framework for business structures draws its authority from the Companies Act 71 of 2008 and sits alongside older, informal structures that SARS still recognises for tax purposes. Before you can make a smart choice, you need to know what options actually exist.

The main company categories under the Companies Act framework include profit companies and non-profit companies. Within profit companies, you have four recognised types: private companies (Pty) Ltd, public companies (Ltd), personal liability companies (Inc), and state-owned companies (SOC Ltd). Outside the Companies Act, sole proprietorships and partnerships are legally recognised for SARS purposes, though they carry no separate legal personality.

A critical misconception: many new business owners assume that close corporations (CCs) are still available for registration. They are not. No new CCs can be incorporated under the current Companies Act. Existing CCs may continue to operate and may convert to one of the recognised profit company types, but you cannot start a new CC today. This surprises a surprising number of entrepreneurs who remember the CC’s simplicity from an earlier era.

Before diving into detailed comparisons, here is a quick snapshot of the main structures available to South African SME owners:

| Entity type | Separate legal person | Limited liability | Ideal for |

|---|---|---|---|

| Sole proprietorship | No | No | Freelancers, micro businesses |

| Partnership | No | No | Two or more co-owners |

| Private company (Pty) Ltd | Yes | Yes | Most SMEs and startups |

| Personal liability company (Inc) | Yes | No (directors liable) | Professionals (lawyers, accountants) |

| Public company (Ltd) | Yes | Yes | Businesses seeking public investment |

| Non-profit company (NPC) | Yes | Yes | NGOs, associations |

| State-owned company (SOC Ltd) | Yes | Yes | Government enterprises |

If you want to understand the business registration steps for each of these types, the process differs meaningfully depending on which structure you choose.

- Sole proprietorship: Easiest to start, no registration with CIPC required, but total personal exposure.

- Partnership: Flexible, no formal incorporation, but all partners share unlimited liability.

- Private company (Pty) Ltd: Most popular for SMEs, offers limited liability, relatively straightforward CIPC registration.

- Personal liability company (Inc): Used by regulated professionals; directors remain personally liable for professional debts.

- Non-profit company (NPC): Income cannot be distributed to members; ideal for civil society organisations.

Choosing between these structures is not just a legal formality. It is a strategic decision that shapes the best business structure choices for long-term growth, investor readiness, and tax efficiency.

Comparing liability and tax for each entity type

Understanding the types is only half the job. What really matters is how each structure treats your personal risk and your tax bill.

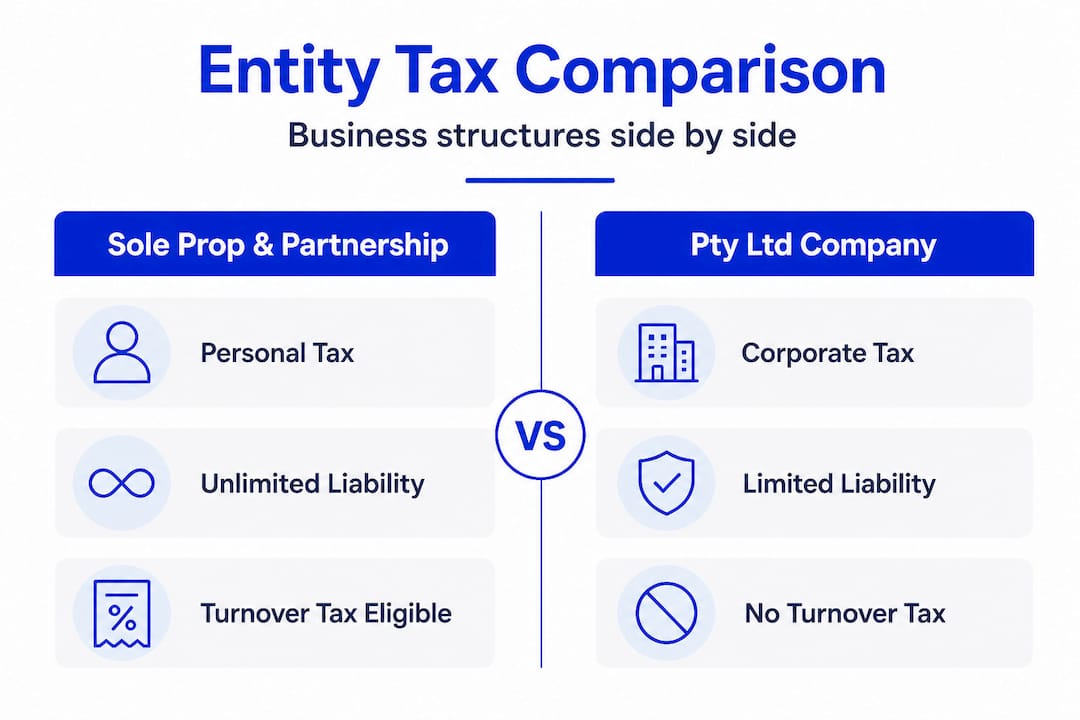

A sole proprietorship is not separate from its owner as a legal person. This means that if your business accumulates debts, creditors can come after your house, your car, and your personal bank account. Business income flows directly into your personal income tax return and is taxed at your applicable personal tax rates. For low-income earners this can be efficient, but as revenue grows, marginal personal tax rates can hit 45% quickly.

Partnerships face the same exposure on both fronts. The partnership is not a taxpayer in its own right. Each partner declares their share of the profits in their own personal income tax return, and each partner faces unlimited liability. What many owners miss is that unlimited liability in a partnership extends to the acts of your co-partner. If your partner makes a bad business decision that results in a lawsuit, you could be personally liable for the full amount, not just your share.

Private companies (Pty) Ltd change this picture entirely. The company is a separate legal person, pays corporate income tax at the flat rate of 27% on taxable income, and generally protects its shareholders’ personal assets. Your personal liability is limited to your shareholding unless you sign personal suretyship agreements with lenders, which many banks unfortunately still require for small businesses.

Here is a comparison of the tax and liability reality across the most common structures:

| Entity type | Tax treatment | Owner’s personal liability | Compliance burden |

|---|---|---|---|

| Sole proprietorship | Owner’s personal tax return | Unlimited | Low |

| Partnership | Each partner’s personal return | Unlimited (joint and several) | Low to moderate |

| Private company (Pty) Ltd | Corporate tax (27%) | Limited to shareholding | Moderate to high |

| Personal liability company (Inc) | Corporate tax (27%) | Directors liable professionally | Moderate to high |

| Non-profit company (NPC) | Exempt if registered; conditional | Limited | Moderate |

Pro Tip: New owners often register as sole proprietors to save on costs and compliance, then get caught off-guard when a single large contract dispute exposes their personal assets. The “savings” on registration fees can look very small compared to what you stand to lose. If your business carries any meaningful contract risk, a private company is almost always the smarter call.

“The choice between a registered company and an informal business structure is not just about what you pay today. It is about how much you could lose tomorrow.”

You can explore your options for tax efficient business structures in more detail, because the interaction between your entity type and your effective tax rate is one of the most underappreciated levers available to South African SME owners. Understanding income tax return rules specific to your structure will also help you avoid costly errors when filing season arrives.

Registration, SARS compliance, and tax incentives

Choosing the right structure means nothing if you do not execute the registration and compliance steps correctly. Here is a practical sequence for getting your entity properly registered and SARS-compliant.

Step-by-step registration process:

- Decide on your structure based on liability needs, tax goals, and growth plans.

- Reserve your company name with CIPC (Companies and Intellectual Property Commission) through their online portal.

- Incorporate with CIPC by filing your memorandum of incorporation (MOI) for companies, or simply proceed with a partnership agreement or no formal document for a sole proprietorship.

- Register for a tax reference number with SARS. As soon as you commence a business, you are legally required to register as a taxpayer with SARS and obtain your reference number.

- Register for VAT if your taxable turnover exceeds or is expected to exceed R1 million in any 12-month period.

- Register for PAYE (Pay As You Earn) if you employ staff.

- Register for UIF (Unemployment Insurance Fund) contributions if applicable.

- Open a dedicated business bank account to maintain clear separation between business and personal finances.

Pro Tip: You must register as a taxpayer with SARS within 21 business days of starting business activities. Missing this window opens you up to penalties that are entirely avoidable.

One of the most valuable but underused tax tools for new businesses is the turnover tax system. Turnover tax is designed for qualifying small businesses with yearly turnover of R1 million or less. It replaces normal income tax, capital gains tax, and secondary tax on dividends with a single simplified calculation based on turnover rather than profit. It is available to sole proprietors, partnerships, close corporations, companies, and co-operatives.

For businesses just starting out or operating with thin margins, turnover tax can dramatically reduce the administrative burden of tax compliance and sometimes the actual tax bill itself. Not every business qualifies though; businesses in certain professional or financial service categories are excluded.

Common compliance missteps that delay or derail new businesses:

- Failing to register with SARS within the required 21-day window.

- Mixing personal and business finances, which creates a nightmare during audits.

- Not filing annual returns with CIPC, which can lead to deregistration of your company.

- Ignoring VAT registration thresholds until SARS triggers a retrospective audit.

- Assuming that a verbal partnership agreement provides any meaningful legal protection.

Both registering your business and managing small business tax essentials become far less intimidating once you have a clear sequence to follow rather than treating compliance as a series of ad hoc tasks.

When to choose which entity: Practical considerations

Real business decisions are messier than any framework. Here is how common owner scenarios map to the right entity choice.

Single owner, low risk: A graphic designer or consultant with no employees and low contract values can reasonably start as a sole proprietor, register with SARS, and operate simply. But if that designer starts winning large corporate contracts, the liability exposure becomes a real risk. Moving to a private company at that point is a smart, relatively low-cost upgrade.

Two co-founders: A partnership can work for a short time, but the unlimited joint and several liability issue is serious. Two founders building anything with scale potential should incorporate as a private company and formalise shareholding from the start. This also makes investor conversations far simpler later.

Startup with plans to scale and raise funding: There is essentially only one sensible choice here: a private company (Pty) Ltd. Investors cannot take equity in a sole proprietorship or partnership. Venture capital and angel investors in South Africa expect a properly registered company with a share register, a MOI, and auditable financial records.

Legacy CC holder: If you are operating an existing close corporation, you have a decision to make. You cannot register a new CC, but existing CCs can convert to a profit company type. Whether and when to convert depends on your specific tax position, the composition of your members, and your growth plans. Many CC owners delay this unnecessarily, missing out on the governance and funding advantages of a proper company structure. Exploring the company registration framework will give you clarity on the conversion path.

Factors to weigh when choosing your structure:

- Scale: How large do you expect the business to grow in the next five years?

- Liability: Are you signing contracts, employing people, or holding assets that could attract claims?

- Funding: Will you ever need external investment or a formal business loan?

- Compliance burden: Do you have the capacity (or budget for advisors) to handle company-level compliance?

- Succession: What happens to the business if an owner exits, retires, or passes away?

Pro Tip: Start with the simplest structure that gives you the protection you need today, but document your intended growth path. Revisiting your structure when your revenue doubles or when you bring on investors is not a failure. It is good planning.

The uncomfortable truth about business structures in South Africa

Here is something most guides will not tell you: picking a business entity is not a once-off administrative step you complete at startup and forget. We have seen it repeatedly in the businesses we work with. An owner registers a sole proprietorship because it is cheap and easy, grows the business to R4 million in annual revenue, and then faces the painful and expensive process of restructuring because the tax and liability consequences of the original choice are now actively working against them.

Entity selection is a continuing strategic decision. Your structure should evolve as your business evolves. The personal tax rates that apply to a sole proprietor start to bite hard above certain income thresholds, while a private company with a well-structured salary and dividend split can legally reduce the same owner’s effective tax rate by a significant margin. These are not loopholes. They are the deliberate outcomes of choosing the right structure for your size and stage.

The real risk most SME owners carry is not a single bad decision. It is the compounding cost of the wrong decision left in place for too long. Unlimited liability from a sole proprietorship or partnership can feel theoretical until a supplier dispute or a customer injury claim lands on your personal doorstep. By then, the window for easy restructuring has often passed.

Our honest recommendation is to revisit your business structure every two to three years, or any time you hit a major milestone like your first employee, your first large contract, or your first approach from an investor. What worked at launch will often constrain you later. Reviewing your long-term structure planning with professional support is one of the highest-return activities you can invest in as a business owner.

How expert support can simplify structuring and compliance

Navigating entity selection, CIPC registration, SARS compliance, and ongoing tax obligations without expert support costs most SME owners far more in time, errors, and missed opportunities than the cost of getting proper help. At Ready Accounting, we engineer your financial infrastructure from the ground up, including identifying the right entity structure for your specific growth trajectory, automating your compliance workflows, and building real-time financial visibility into your business. Our approach to accounting automation removes the manual friction that bogs down most SMEs, while our tax strategy work actively helps you reduce your tax liability through legal, structure-driven planning. If your business is growing and your current setup is starting to feel like it is working against you, that is exactly the moment to talk to us.

Frequently asked questions

Can I still start a close corporation in South Africa?

No, new close corporations cannot be formed under the Companies Act, but existing CCs may continue operating or convert to a recognised profit company type.

What is the main benefit of registering as a private company (Pty) Ltd?

The major benefit is limited liability and separate legal personality, meaning your personal assets are generally protected if the business faces debts or legal claims.

Who pays tax in a partnership?

Each partner is taxed on their share of the profits in their own personal income tax return, and each partner faces unlimited liability for business debts. The partnership itself is not a taxpayer.

What is turnover tax and who can use it?

Turnover tax applies to businesses with annual turnover of R1 million or less, and is available to sole proprietors, partnerships, companies, close corporations, and co-operatives as a simplified alternative to normal income tax.

How soon must I register my business with SARS?

You must register as a taxpayer with SARS within 21 business days of commencing business activities to avoid penalties.