Master cash flow management for South African SMEs

Executive Summary

- Effective cash flow management prevents profitable businesses from failure due to cash shortages.

- Regular tracking, forecasting, and disciplined collections are essential for South African SMEs.

- Automating cash flow practices and maintaining reserves increase resilience against unpredictable costs and delays.

Profitable businesses fail every year in South Africa, not because they lack customers or revenue, but because cash simply runs out before the next invoice clears. Cash flow management is the practice of tracking, forecasting, and controlling the movement of actual money into and out of your business, making sure you always have enough on hand to cover wages, suppliers, and tax obligations. For South African SMEs operating in an environment of delayed payments, load-shedding costs, and unpredictable demand cycles, mastering this discipline is the single most powerful thing you can do to protect everything you have built.

Table of Contents

- Why cash flow management matters for South African SMEs

- The fundamentals: How cash flow management works

- Core tools and metrics for managing cash flow

- Common challenges and how to stay resilient

- What most SME owners overlook about cash flow management

- How Ready Accounting can transform your cash flow management

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Cash flow beats profit | Strong cash flow is a better survival metric than profit for South African SMEs. |

| Forecast regularly | Updating cash flow forecasts and reviewing them weekly spots issues early and enables quick action. |

| Monitor liquidity ratios | Key ratios like current and quick ratio should always be above 1 to ensure obligations can be met. |

| Keep a cash buffer | Reserve at least a month’s expenses in cash to weather market uncertainty and surprises. |

| Tackle debtor delays | Actively monitoring and collecting accounts receivable strengthens your cash position. |

Why cash flow management matters for South African SMEs

Most SME owners track their profit and loss statement and assume it tells the whole story. It does not. You can show a healthy net profit at the end of the quarter and still be unable to pay salaries on Friday. This gap between profit on paper and cash in the bank is where businesses quietly collapse.

South African businesses experience cash delays and debtors’ constraints that make cash flow management vital in ways that business owners in more stable economies simply do not face. When a large corporate client stretches payment terms to 90 days, your costs do not pause. Suppliers want payment in 30, employees expect wages monthly, and SARS operates on its own fixed calendar.

The local landscape creates specific pressure points that compound quickly:

- Debtor delays: Large clients routinely pay 60 to 90 days after invoicing, creating a dangerous mismatch between when you earn and when you receive.

- Lumpy revenue cycles: Many SMEs in construction, retail, and professional services earn unevenly across months, with feast and famine periods that demand careful planning.

- Unplanned operational costs: Backup power infrastructure, vehicle repairs, and equipment failures hit without warning and drain reserves fast.

- Seasonal fluctuations: Hospitality, agriculture, and retail businesses face predictable but often under-planned seasonal drops in income.

“Cash flow is the lifeblood of any business. Without it, even a company with strong sales and solid profits can be forced to close its doors.” This is not a warning for struggling businesses. It is a warning for growing ones.

Effective cash flow management means seeing problems before they arrive. Connecting your budgeting for SME growth to your cash planning creates a single, coherent picture of your financial position rather than two separate documents that never quite agree.

Pro Tip: Build a rolling 13-week cash flow calendar and update it every Monday morning. This single habit gives you more financial control than most fancy software tools ever will.

The fundamentals: How cash flow management works

Once you accept that profit and cash are different things, the next step is building a system that tracks both and bridges the gap between them. Cash flow management is not a once-a-year exercise. It is a living, weekly process built on four core activities.

-

Track every receipt and payment. Record all incoming cash, customer payments, loan drawdowns, grants, and all outgoing cash, supplier invoices, payroll, tax payments, and loan repayments, as they actually clear your bank, not when they are invoiced.

-

Forecast future inflows and outflows. Use your historical data, confirmed orders, and known expense cycles to project what your bank balance will look like three months from now. A cash flow forecasting approach helps you predict timing and amounts of inflows and outflows so you can avoid shortfalls before they happen.

-

Adjust for timing mismatches. If you know a large expense is coming in week six but payment from a client lands in week eight, you need to either accelerate the client payment or arrange a short-term facility to bridge the two weeks. Spotting this two months out is manageable. Spotting it two days out is a crisis.

-

Ensure reserves are adequate. Operating without a cash buffer is the equivalent of driving without a spare tyre. Most SMEs should target at least four to six weeks of operating expenses sitting in a readily accessible account.

Scenario planning adds a powerful layer of resilience. Run three versions of your cash flow projection each month: a best case where clients pay on time and sales hit target, a base case using realistic averages, and a worst case where your biggest client pays 30 days late and a surprise expense hits. When you can answer “what happens if my biggest client goes quiet for 60 days?” without panicking, you are managing cash flow at a professional level.

Your income statement feeds into this process by showing you where margins are being compressed, which helps you anticipate periods when even good sales volumes will not generate strong cash.

Pro Tip: Switch from monthly to three-month rolling projections and update them weekly. Monthly projections give you a rear-view mirror. Rolling projections give you a windshield.

Core tools and metrics for managing cash flow

Understanding the principles is one thing. Having the right instruments on your dashboard is another. These are the tools and metrics that experienced SME finance teams use every single day.

Essential reports and documents:

- Cash flow statement: Shows actual cash received and paid over a period, separate from the profit and loss. The statement of cash flows is divided into operating, investing, and financing activities.

- 13-week cash flow forecast: Your forward-looking projection, updated weekly, using confirmed bookings and known expense schedules.

- Debtors age analysis: A breakdown of all outstanding invoices by how long they have been unpaid (30, 60, 90+ days). This tells you exactly where your cash is sitting idle.

- Creditors schedule: A list of all amounts you owe, with due dates, so you can plan outflows and avoid late payment penalties.

Key metrics to monitor every week:

Monitoring liquidity ratios such as the current ratio and quick ratio is a concrete way to know whether your short-term obligations are covered at any given moment.

| Metric | What it measures | Healthy target |

|---|---|---|

| Current ratio | Current assets divided by current liabilities | Above 1.5:1 |

| Quick ratio | Liquid assets only, divided by current liabilities | Above 1:1 |

| Debtor days | Average number of days to collect payment | Under 45 days |

| Creditor days | Average days before you pay suppliers | 30 to 60 days |

| Cash burn rate | Monthly operating cash outflow | Know your number |

| Cash runway | Months of cash remaining at current burn | Minimum 3 months |

A healthy current ratio means you have more assets available in the short term than you have bills due. The quick ratio is stricter because it excludes stock, which may take time to convert into cash. Both ratios should sit above 1:1 and you should monitor them as part of your key SME financial KPIs every single month.

Using bank statement analysis tools can automate a large portion of the data-gathering process, turning raw transaction data into categorised cash flow patterns that would otherwise take hours to compile manually.

Statistic to know: Research consistently shows that cash flow problems are among the top three reasons SMEs fail globally, and South Africa’s long debtor payment cycles make this risk even more acute for local businesses.

Common challenges and how to stay resilient

Knowing the tools is important. Knowing where things tend to break down is equally important. South African SMEs face a set of recurring cash flow traps that follow predictable patterns once you know what to look for.

The most common challenges include:

- Client payment delays that stretch well beyond agreed terms

- Unplanned capital expenses hitting during slow revenue periods

- Tax payments arriving as a shock because VAT and provisional tax were not budgeted monthly

- Rapid growth consuming cash faster than new revenue covers it

Resilience comes from having both systems and discipline in place before a crisis hits. Here is a practical sequence for building that resilience:

-

Set up a dedicated cash buffer account. Transfer a fixed percentage of every payment received into a separate account reserved for emergencies. Treat it like a fixed expense, not optional savings.

-

Tighten your collections process. Send invoices immediately on delivery. Follow up on day 31 for any unpaid invoices. Do not wait until day 60 to start chasing. Every day of delay costs you real money. Reviewing common cash flow issues will show you exactly how debtor management links to your overall cash position.

-

Align payroll timing with cash inflows. If your biggest clients pay mid-month, consider structuring payroll timing to follow that pattern rather than running payroll at month-end when the bank account is at its lowest.

-

Budget for irregular costs monthly. Annual insurance renewals, vehicle licences, software subscriptions, and equipment servicing are predictable. Divide the annual total by 12 and set that amount aside each month so the cost never hits as a surprise.

-

Avoid short-term cash advances without a clear repayment plan. Merchant cash advances can provide quick liquidity, but common mistakes with cash advances often lead businesses into a cycle of borrowing that worsens the underlying cash problem.

Maintaining a cash buffer for at least one month puts your business ahead of the majority of SMEs and gives you the time to respond to problems rather than react to them in panic.

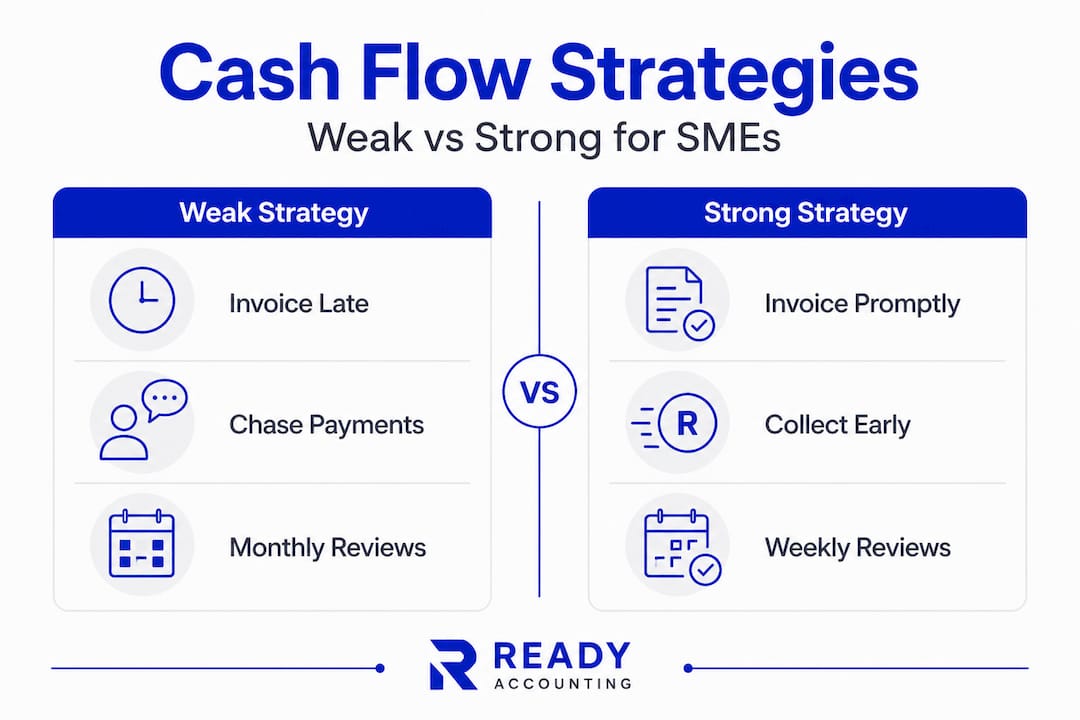

| Weak cash flow strategy | Strong cash flow strategy |

|---|---|

| Invoice at month-end | Invoice on delivery |

| Chase debtors after 60 days | Chase debtors on day 31 |

| No cash reserve | 4 to 6 weeks of expenses in reserve |

| Monthly cash review | Weekly rolling forecast |

| Budget profit only | Budget cash separately from profit |

| React to shortfalls | Forecast and prevent shortfalls |

The discipline of weekly reviews and structured collections is not glamorous. But it is the difference between a business that survives a slow quarter and one that does not. Thinking about boosting profitability alongside cash management ensures that revenue improvements actually translate into cash improvements, not just larger receivables balances.

What most SME owners overlook about cash flow management

Here is the part that most financial articles skip. Business owners pour hours into reviewing their profit margins, chasing revenue growth, and optimising pricing. They spend almost no time on collections rhythm and cash timing. This is backwards.

The single most impactful thing most SMEs can do right now costs nothing and requires no software. Chase every overdue invoice the moment it becomes overdue. Not a reminder on day 60. A firm, professional call on day 31. The businesses we work with that make this one behavioural change consistently see their debtor days drop by 15 to 25 days within a quarter. That is weeks of cash freed up without a single new customer.

The second thing people overlook is that automation is not a replacement for discipline. Cloud accounting platforms are genuinely powerful. Real-time dashboards give you instant visibility. But we have seen businesses with excellent technology still run into cash crises because nobody actually looked at the dashboard and acted on what it showed. Tools amplify good habits. They cannot create them.

The uncomfortable truth about cash flow challenges is that they are almost always predictable in hindsight. The warning signs were there in the debtor age analysis weeks before the crisis hit. The gap between seeing a warning and acting on it is where most SME owners lose time they cannot afford.

Make cash flow review a weekly team ritual, not a solo finance exercise. When your operations manager knows the cash position, they make better decisions about accepting urgent orders or committing to supplier deals. Cash flow awareness embedded in your team culture is a genuine competitive advantage.

Pro Tip: Frame cash to your team as oxygen. You can survive a few uncomfortable weeks with thin margins. You cannot survive a single week with no cash. Weekly cash flow conversations shift the whole team’s thinking from revenue-first to sustainability-first.

How Ready Accounting can transform your cash flow management

Managing cash flow manually across spreadsheets, bank statements, and disconnected systems drains hours every week and leaves too much room for error. Ready Accounting replaces that friction with automated cash flow management built on custom cloud infrastructure, real-time runway dashboards, and API integrations that connect your bank, invoicing, and payroll into a single live picture. You stop chasing historical data and start making decisions based on what your cash position looks like right now and three months from now. If you are ready to stop guessing and start governing your cash with precision, explore our accounting automation guide to see exactly how we build these systems for South African SMEs and what the results look like in practice.

Frequently asked questions

What is the main difference between profit and cash flow?

Profit is the accounting surplus after expenses are deducted from revenue, while cash flow tracks real money physically moving in and out of your bank account. You can be profitable on paper while being unable to pay a supplier tomorrow if your debtors have not settled yet.

How often should I review my SME’s cash flow?

Review your cash flow projections at least once a week and update your forecast immediately when a major payment changes or a new expense is confirmed. A cash flow forecast can show bumps in the road long before you hit them, but only if you keep it current.

What are the most important cash flow ratios to track?

The current ratio and quick ratio are your most critical indicators. Both should stay above 1:1 to confirm your SME can meet short-term obligations, with the current ratio ideally sitting at 1.5:1 or higher for a comfortable buffer.

How much cash buffer should an SME keep?

Aim to hold at least one month of operating expenses in a dedicated reserve account. Knowing you have enough cash for a month gives you breathing room to respond rather than react when an unexpected cost or payment delay hits.

Recommended

- Income statement guide for South African SMEs | Ready Accounting

- Why budgeting matters for South African SME growth | Ready Accounting

- Financial forecasting: a practical guide for SA SMEs | Ready Accounting

- Outsourced CFO services for South African SMEs: grow faster | Ready Accounting

- Practical business cash flow management steps for UK SMEs